Volatility in global energy markets intensified on Tuesday, with prices falling across the board – especially in Europe, where futures reversed their gains over the previous two trading sessions, and in the US, where the April contract expired after a day of drama.

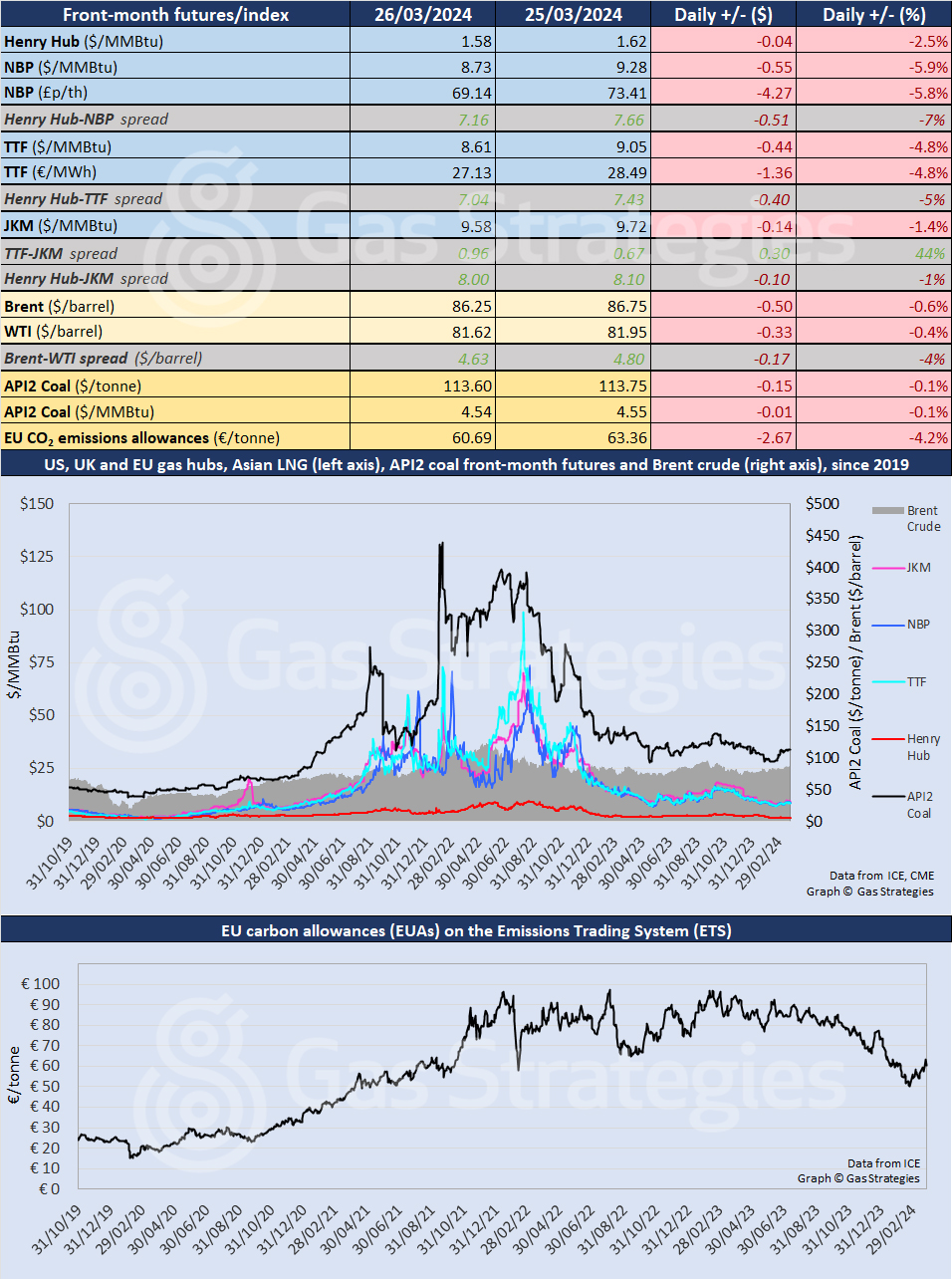

In continental Europe, the front-month TTF contract was down 4.8%, from USD 9.05/MMBtu on Monday to USD 8.61/MMBtu on Tuesday, mostly reversing the gains of the previous two sessions. Despite the fall, the underlying upwards trend of the past month, from a low reached on 23 February, remains evident.

UK gas futures moved a little more sharply than TTF, with NBP down 5.9%, from USD 9.28/MMBtu to USD 8.73/MMBtu.

Prices remained volatile on Wednesday morning but were back to around Tuesday’s closes by lunchtime in London.

The underlying price rise of recent weeks comes despite warming weather and historically high storage levels. With spring getting into its stride after the vernal equinox last week, data from Gas Infrastructure Europe (DIE) show EU facilities were still 59.0% full on Monday. This compares with 53% a year ago and 26% two years ago.

In the UK, GIE data show storage at 38.6% full, compared with 58% a year ago and 26% two years ago. UK storage is more volatile than in the EU because capacity is low relative to peak demand.

GIE data show EU storage changes over the past week have been mainly withdrawals but of low magnitude either way.

In Asia, the JKM LNG price fell by 1.4%, from USD 9.72/MMBtu on Monday to USD 9.58/MMBtu on Tuesday. The TTF-JKM spread widened to USD 0.96/MMBtu, its highest level since mid-February.

Commodities trader Vitol yesterday reported that its LNG volumes grew by 24% in 2023, with CEO Russell Hardy commenting that “120 Bcm/year of Russian pipeline gas which used to flow to Europe has, to date, been replaced by an additional 62 Bcm/year of LNG and significant demand destruction”. Vitol’s natural gas trading volumes were up 19%.

In the US, the Henry Hub April contract expired at USD 1.58/MMBtu on Tuesday after falling 2.5% from USD 1.62/MMBtu on Monday – its fifth consecutive fall – following significant intra-day volatility.

The new front-month May contract, which closed at USD 1.79/MMBtu on Tuesday, was trading at around USD 1.75/MMBtu on Wednesday morning.

Crude oil prices moved downwards after Monday’s rally, with Brent falling by 0.6% from USD 86.75/barrel to USD 86.25/barrel, and WTI down 0.4%, from USD 81.95/barrel to USD 81.62/barrel.

European carbon prices fell sharply, with EU emissions allowances down 4.2%, from EUR 63.36/tonne on Monday to EUR 60.69/tonne on Tuesday, reversing much of the previous session’s rise.

API2 coal remained elevated but flat at USD 4.54/MMBtu.

Front-month futures and indexes at last close with day-on-day:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.