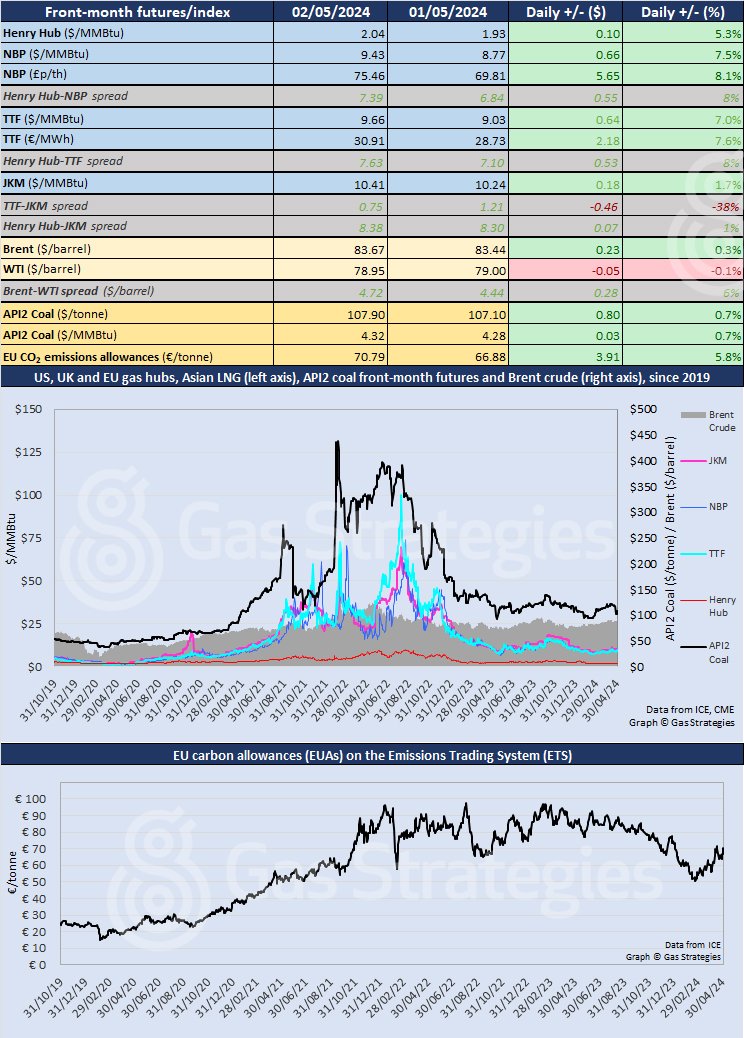

Natural gas futures in all of the main consuming regions were up on Thursday, with European prices particularly volatile, jumping by around 8% in local currencies. In the US, front-month Henry Hub rose above USD 2/MMBtu following the latest government data on storage levels, while the Asian JKM LNG price was up by nearly 2%.

Crude oil price movements were muted after Wednesday’s dramatic falls.

Yesterday’s rises in European gas prices were a continuation of a sawtooth pattern that has lasted for around a fortnight, but the magnitude of the rise took prices to where they last were on 19 April, in the immediate aftermath of Israel’s retaliation for Iran’s direct drone and missile attack in the middle of April.

It was not immediately obvious why prices moved so sharply, given that there was little obvious support from market fundamentals.

In continental Europe, the June TTF contract was up 7.0%, from USD 9.03/MMBtu on Wednesday to USD 9.66/MMBtu on Thursday. In local currency terms, the rise was 7.6%. The price opened higher on Friday morning but then started to decline.

In the UK, NBP jumped by 7.5%, from USD 8.77/MMBtu to USD 9.43/MMBtu. In local currency, the rise was 8.1%. Its trajectory on Friday morning was similar to that of TTF.

In Asia, JKM rose by 1.7%, from USD 10.24/MMBtu on Wednesday to USD 10.41/MMBtu on Thursday, more than reversing the fall in the previous session and narrowing the TTF-JKM spread to USD 0.75/MMBtu. Like the European contracts, JKM has been in a sawtooth pattern since 19 April, but in a much less volatile range of USD 10.21-10.53/MMBtu.

In the US, front-month Henry Hub jumped 5.3%, from USD 1.93/MMBtu on Wednesday to close at USD 2.04/MMBtu on Thursday, following publication earlier in the day by the Energy Information Administration (EIA) of weekly storage data.

The EIA estimated working gas in storage at 2,484 Bcf as of 26 April, up 59 Bcf from the previous week and above the five-year historical range. Stocks were 436 Bcf higher year-on-year and 642 Bcf – or 35% – above the five-year average of 1,842 Bcf for this time of year.

Other factors in the rise were increasing supply to the Freeport LNG export plant and expectations of warmer weather to come.

Crude oil prices diverged, with Brent up 0.3% to USD 83.67/barrel and WTI down 0.1% to USD 78.95/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.