In our recent LNG infrastructure transaction work, one question has come up more than any other from investors - “how should we think about decarbonisation?”. As we pass the peak of the Coronavirus pandemic and begin to cast an eye to the future recovery pathway, this question is more pertinent than ever. One school of thought suggests decarbonisation could fall by the wayside, at least temporarily, replaced by a laser-focus on stimulating economic growth and job creation powered by low priced fossil fuels. However, others see an opportunity to accelerate the transition and build upon the low-emissions silver lining seen during widespread lockdowns. It has been suggested government support during the recovery could be channelled towards green industries, for example.

From our conversations with several funds over the past weeks, we are aware that capital is available, and they are hungry for opportunities to be able to deploy this despite the economic climate[1]. Guaranteed revenue, long term contract backed, assets such as US liquefaction projects could emerge as a favoured asset type for investors looking for reliable returns in the energy sector during a time of huge commodity price uncertainty. This is illustrated by Cheniere’s above market share price rise during a period of falling LNG prices and growing threat of cancelled LNG cargos.

The question of decarbonisation is especially relevant for assets with long term contracts like US liquefaction projects. With a long, typically 20-year, period where revenues are well understood, these transactions can be won and lost based on how liquefaction capacity is valued post contract expiry.

It is important that the long-term value impact of decarbonisation doesn’t get overlooked if greater focus in due diligence is given to understanding increased short term market uncertainty. Decision makers and investment committees should be asking questions. New targets are being set on a regular basis by companies and countries aiming to reach “net zero” [2] over the next 10-30 years. What will this period look like? Will these targets be met, or re-evaluated after COVID-19? What will this mean for gas or LNG demand? And, most critically, how should this be reflected in the valuation of an asset?

The narrative can be very confusing. Does decarbonisation present an upside, or downside, risk for gas? The common narrative is that of gas as a ‘fuel for the energy transition’, with a bigger role in a low carbon world. In some senses, this is true; coal to gas switching is already in full swing in Europe and the US. In large, coal dependent, markets such as China and India, gas demand would be considerably higher in a decarbonised world.

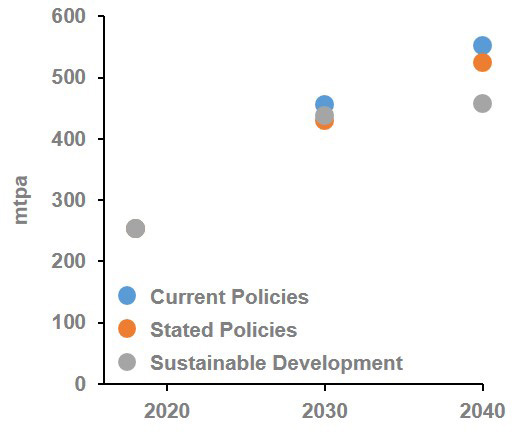

Figure 1 - IEA LNG Trade Forecasts

Source: IEA WEO 2019

Source: IEA WEO 2019

However, for the most part, a degree of decarbonisation is a downside risk to gas demand. Most market forecasts, including our own, expect LNG demand to be 650-700mtpa by 2040, from just under 360mtpa in 2019. The IEA forecasts inter-regional LNG trade, which omits some intra-regional flows to give a slightly lower forecasts, but their work gives a good indication on demand trajectory under different decarbonisation scenarios. In the IEAs “Sustainable Development Scenario (SDS)” (which is consistent with the COP 21 goal and limits temperature increases to 1.6 C), LNG demand in 2040 lies a third lower at 460mtpa, a significant downside. This divergence happens mainly in the 2030-2040 period, with the 2030 SDS forecast not dissimilar to Current Policies Scenario, and above the Stated Policies Scenario. These scenarios were developed before the COVID-19 pandemic, however the long term link between decarbonisation and LNG demand should remain valid.

Much of this downside risk sits in Europe, where a more rapid shift to renewables, green gases and hydrogen could see LNG imports wiped out entirely during the 2030s. If the coronavirus pandemic does develop into a catalyst for decarbonisation, it will be in the developed markets of Europe where this is most profound, further supporting this. The reduction and eventual cessation of LNG imports into Europe directly challenges the thesis that LNG demand grows as indigenous production falls away. This would put an end to Europe’s role as the “sink” market for LNG.

So, to the important question. What does this mean for asset valuations? Even in a decarbonised world, LNG demand is still forecast to be over 100mtpa higher than it is today. It is still growing, and ageing plants will be retiring, increasing the overall addressable demand for LNG exporters. In this scenario, today’s liquefaction capacity, and more, will be needed. Based on this, new build plants would set the price for capacity, so a plant with its capital investment fully amortized by the mid or late 2030’s will be able to capture significant value from new off-take or tolling contracts.

However, it is a fine balance. Further large supply investments, or lower demand driven by more rapid decarbonisation, would change the picture. It doesn’t take a lot to tip the balance to an oversupplied world, with significant competition for contracts, where prices may be set on a cost-plus basis, and where there is a risk of shut-ins or closures.

Complicating this picture is the risk that cyclicality poses. While investments in LNG, like any capital-intensive industry, will always face this risk, LNG is heading into a particularly volatile future. The behaviour of major resource holders could amplify this. Decarbonisation may create an imperative for them to produce gas today while it still has value rather than wait for a future where it may no longer be needed. This could lead to further over-capacity as nations race to produce their resources before the world decarbonises.

Looking at macro scenarios alone is not enough to make sense of such complex, interlinked, possible futures. Risks will be different for different assets and in different time periods, and valuations need to reflect this. Through our due diligence work, we help clients unpick this complexity, embrace rather than fear the uncertainty, and assess how these complex factors will really impact the specific assets they are considering.

For example of our work on complex infrastructure transactions click here

[1] https://www.gasstrategies.com/information-services/lng-business-review/bolt-blue-lngs-growth-spurt-cut-short-covid-19

[2] Carbon neutrality, or having a net zero carbon footprint, refers to achieving net zero carbon dioxide emissions by balancing carbon emissions with carbon removal or simply eliminating carbon emissions altogether

***

If you would like more information about how Gas Strategies can help your business with Consulting services across the value chain or provide industry insight with regular news, features and analysis through Information Services or help with people development through Training Services, please contact us directly.