Will the future of Eastern Mediterranean1 gas development continue to be driven by the export market or are the established gas markets, which already exist within the region, sufficient to sustain investment and new activity? With upstream players and infrastructure investors looking closely at opportunities in the region this is a particularly relevant question – especially in the face of globally weakened commodity prices and slashed capital expenditure budgets threatening investment in potential new large liquefaction projects and international export pipelines.

Introduction

Competing infrastructure solutions, significant upstream discoveries and ongoing exploration campaigns: there is much activity in the East Med gas sector. Many recent headlines covering the region have focused on the multiple proposed projects that seek to export gas from the region with an eye on supplying the large markets in Europe – which sit tantalizingly close across the Mediterranean Sea.

However, the region is a significant consumer of gas in its own right – providing local opportunity to the upstream players seeking to turn gas discoveries into production projects, gas marketers considering where to place their gas, and banks and funds seeking entry via investment in regional gas infrastructure. When considered together with the present challenging investment climate and weakened global gas market; is gas export the only game in town, or is it time the Eastern Mediterranean started playing for keeps with its gas, looking inwards rather than outwards to support continued investment in its gas sector?

Mind the gap

Development of its giant Leviathan and Tamar fields has provided Israel with a surplus of gas, some of which is being exported to Jordan and Egypt, while Egypt – by far the largest producer in the region – has itself also returned to a situation of gas surplus, primarily as a result of the ramp up of production from the supergiant Zohr field. And gas discoveries offshore of Cyprus – together with well-documented ongoing exploration activity – have set that country on track to become a significant gas producer too.

Gas demand in the region is dominated by Egypt, with significant future growth expected, and Israeli gas consumption is also expected to grow significantly in coming years as its indigenous gas resources replace liquid and solid fuels.

A forward-looking view of production from existing fields, and new and potential developments – compared with expected demand growth – suggests that the East Med is moving towards a gas deficit by the end of the present decade. The is shown in our long-term forecast for the region (see Figure 1)2. The exact timing of this deficit is uncertain, as it will depend on whether discoveries progress to development, and whether exploration, which is not shown here, can add further economic volumes.

Figure 1 East Med regional gas supply-demand balance (2020-2040)

Source: Demand - Gas Strategies analysis. LNG Export is the capacity of existing liquefaction facilities (Idku and Damietta). Supply - Gas Strategies analysis of Rystad UCube data

And yet, with global gas prices currently languishing at decade-long lows and the global LNG market expected to remain long throughout most of the 2020s, the focus from developers of new projects continues to be on exporting gas out of the region rather than its utilisation within the East Med itself.

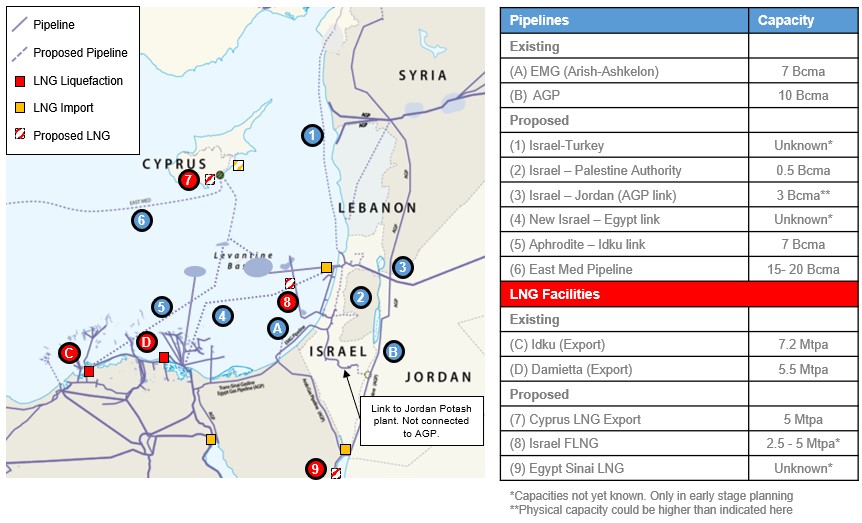

Currently, the only export route is via the LNG export terminals in Egypt. However, cargo output from the Idku terminal has been restricted due to the low prices prevailing in export markets – a price environment that may also lead to a delay in the planned June restart of the idled Damietta plant. Multiple greenfield LNG export projects have been proposed, including in Cyprus, which recently fast-tracked permits for an LNG import project (reinforcing the need for gas in the region). And the largest proposed pipeline projects will either link gas fields to existing LNG plants or directly transport molecules out of the region to Europe (Figure 2).

Figure 2 Existing and proposed gas infrastructure

Source: Gas Strategies additions to Entsog base infrastructure map : ENTSOG TP [17-04-2020] https://transparency.entsog.eu/, Pipeline capacities : Med Reg

Spending slashed and new liquefaction projects put on ice

Enter, then, the largely unforeseen events of this year: energy commodity price crashes coupled with the global economy headed towards a recession the depth of which has not been seen for decades. Capital spending in the oil and gas industry has been slashed, and new projects delayed or cancelled globally. The impact could be especially acute in the East Med as the majority of projects are greenfield developments, the economics of which have been based on export prices to a global market – with assumptions that have been shaken by weakened demand and low prices. As a result, we are already seeing one key regional player coming under financial pressure, another cutting exploration campaigns and deferring developments, and the Majors reviewing planned activities in Cyprus.

The implications of this are self-reinforcing. Delay of upstream projects brings forward the potential regional gas deficit. So too does diminished exploration, which also reduces the likelihood of a ‘black swan’ event like another Zohr-type discovery dramatically changing the balance.

Inwards-looking investment opportunities

So, where do the best opportunities lie in an ‘inward looking’ East Med? Regional interconnectivity remains critical. Gas will need to be transported from Israel (and potentially Cyprus) to Egypt, as the largest regional gas market. The existing EMG pipeline – which has recently restarted following flow reversal – and the AGP pipeline could both serve a key role in moving gas from Israel to Egypt, with brownfield infrastructure providing by far the most cost effective transport option.

That said, the regional market (particularly in Egypt) is not without its own challenges. A perceived lack of creditworthy buyers, and domestic prices for most customers at a level less than an LNG netback, have been the rationale for so much ‘looking out’ at export. Liberalization of the gas market has been written into law but is yet to truly happen. Market-based logic suggests these issues should resolve as the gas deficit emerges and market fundamentals support a need for gas imports. However, this was not the case when Egypt imported gas in the past. Looking inwards at the regional market still needs to be done with consideration.

Gas Strategies sees the opportunity for infrastructure ownership shakeups, as pipelines are now serving a different market and purpose to their original intention when some of the current owners invested. And there are examples of existing infrastructure owners previously seeking to sell their interests on falling revenues triggered by the previous oil price crash.

The need for new infrastructure also remains. A connection from offshore Cyprus (and potentially Israel) to Egypt is perhaps the most likely major new pipeline and is backed by strong market fundamentals. But the appetite for developing such a route in the near future is likely to be low, given the current economic conditions. Infrastructure investors are eager for new opportunities in the region, but delayed upstream developments may frustrate the opportunity to invest.

The surplus of gas in the short term and cost competitiveness of brownfield LNG infrastructure in Egypt, even in a low gas price world, will ensure exports will continue to have a role to play in an ‘inward looking’ East Med. However, export is perhaps better thought of as a short- to mid-term upside, on top of a base case focused on the strong regional market, rather than the ultimate and only basis for gas developments in the region.

The East Med already had strong market fundamentals and growing regional demand. Projects were arguably more focused on export than they should have been as companies tried to realise quick returns and avoid regional market complexities. However, now with a weaker export market, and delays to projects, it may well be time for companies and governments in the East Med to looked in rather than out.

1 Or ‘East Med’. In this article we include Egypt, Israel, Jordan and Cyprus as the constituent members of the East Med gas region.

2 This simplified view assumes no infrastructure constraints

***

If you would like more information about how Gas Strategies can help your business with Consulting services across the value chain or provide industry insight with regular news, features and analysis through Information Services or help with people development through Training Services, please contact us directly.