2020 has spawned an abundance of talk, speculation and indeed policy statements on hydrogen. FOMO (fear of missing out) has taken over and governments, investors, utilities, technical and professional services providers alike have been busy looking for ways to plant their flag on this new territory.

However, we have been here before – this is not the first time that hydrogen has been touted as the future of energy. In the wake of the first oil crisis in the 1970s western governments began looking at alternatives to oil. Hydrogen was seen as a perfect alternative produced from plentiful, safe and cheap nuclear energy. However, following the Three Mile Island nuclear accident, and the world adjusting to higher oil prices, the grand plans for the hydrogen economy were quietly shelved. In the 2000s, we saw a resurgence of enthusiasm, particularly for hydrogen as a transport fuel, only to find that by the end of the decade, battery electric vehicles were rapidly winning the technology race and hopes for hydrogen faded.

Today the driver for renewed interest in hydrogen is not energy security but climate change mitigation. The technical solution of hydrogen has found a new problem to address, but so far the challenges to its commercialisation have not received sufficient attention.

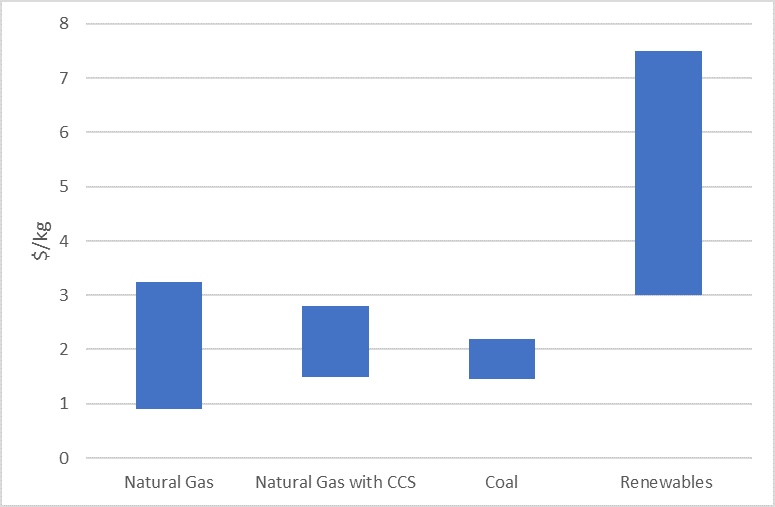

Hydrogen has the clear advantage over fossil fuels of being carbon free. However, the impediments that faced its adoption in the past remain: naturally occurring elemental hydrogen is very scarce on Earth and so it must be manufactured; it has a low energy density compared with fossil fuels; there is very limited infrastructure to produce, transport and consume it; and it is currently extremely expensive to produce whether from natural gas or through electrolysis. The costs of producing green hydrogen using electrolysis today in the US and Europe would be (at the lower end) between $4.00 and $4.50 / kg which is equivalent to $30/MMBtu, 10 times the current US natural gas price and 6 times the current European price. It would need a European ETS price of over €300/tonne – 10 times the prevailing price in 2020 – just to levelise the cost of hydrogen with natural gas today.

Estimated range of hydrogen production costs by technology

Source: The Future of Hydrogen, IEA, June 2019

Source: The Future of Hydrogen, IEA, June 2019

We may accept conventional wisdom that the costs of producing hydrogen will fall as technology develops and the industry matures, as seen elsewhere in the energy industry with the huge drop in the cost of some technologies used in renewable electricity generation. That said, it is likely to be a long time before hydrogen can compete on a purely economic basis with fossil fuels, even allowing for the rise in carbon prices expected by many industry players. So some form of subsidy or government compulsion will be required to make hydrogen projects a reality.

The imperative must be to address the commercial realities

Therefore the greatest potential for early adoption of hydrogen will be in applications where decarbonisation is a strong imperative but renewable electricity is not the solution. These areas are likely to include heavy industry, long distance road, marine and even air transport and storage for renewable electricity.

There remains, however, the complex problem of making that “adoption” happen. This mirrors the challenges we have seen and continue to see in those economies and applications into which natural gas has been introduced over the past 50 years:

- Industry is naturally slow to adopt new technologies within their core business processes

- Even where global peers have proved that the technology works, individual operators need to have confidence that new supply chains will be reliable and sustainable – which encourages a “wait and see” approach

- Meanwhile, potential supply infrastructure projects are unable to proceed in the absence of assured offtake and revenue to underpin financing

Government subsidy or compulsion of themselves do not resolve these commercial issues.

For the global gas and LNG industry, the past 10 years has yielded a great deal of experience in the challenges of opening up new markets – and of the enormous difference between what is feasible and what is realisable. For hydrogen, this may be a case of addressing the risks of a new technology instead of the LNG import challenges of integrating with a global supply chain and commodity price risk. The analogues and the opportunity to learn from the mistakes and successes of others should not be missed by those seeking to build the hydrogen economy.

It is perhaps not surprising that the most advanced opportunities for a prospective investor to consider are being developed to address emissions from industries where electricity is not a ready substitute. Industrials are forming partnerships with major energy players in arrangements that combine supply chain assurance for the hydrogen offtaker and reciprocal anchor customer revenue assurance to the project. It is a symbiotic relationship. A number of the most advanced large-scale projects are in Europe (although there are many others across the world) and focus on decarbonising large industrial hubs where CO2 emissions are highest. They often combine Carbon Capture, Utilisation and Storage (CCUS) projects for industries that will continue to use fossil fuels with green or low carbon hydrogen production where the hydrogen will be used for both for existing consumers (fertilisers / refining) and new consumers where it will substitute for natural gas and other fossil fuels.

The liberalised energy markets in Europe provide no market signal for hydrogen investment

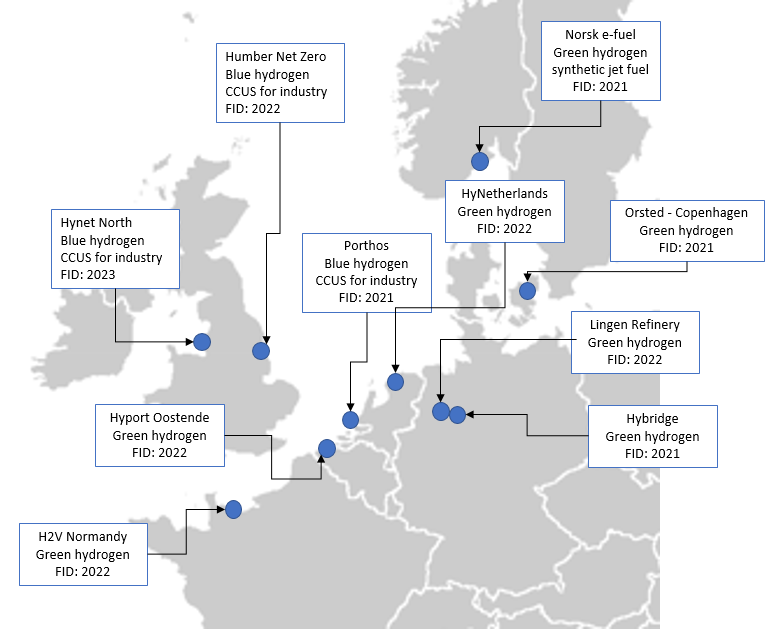

The map below shows a selection of the proposed projects in North West Europe which are aiming to be up and running before 2025. FID years are estimates based on what has been stated by the projects:

Proposed Hydrogen and CCUS project in North West European Industrial Zones

Source: IEA Hydrogen project database and Gas Strategies research

Source: IEA Hydrogen project database and Gas Strategies research

In addition to these larger industrial scale projects we are also likely to see a number of smaller green hydrogen production facilities established associated with pilot schemes for transport fueling (for example for municipal bus fleets and long-haul trucking) and pilot schemes for hydrogen production and storage as a way to offset the intermittency of renewable electricity production.

The adoption of hydrogen as a substitute for natural gas appears to be well outside normal commercial planning timelines. The liberalised energy markets in Europe provide no market signal for hydrogen investment: CO2 prices on their own are too low to offer reliable support and there is no incentive for customers – particularly industrial customers – to unilaterally switch to a fuel that would render their businesses uncompetitive.

Investment and revenue support schemes will therefore be essential to unlock project development. The models that have been used for renewable electricity development over the years may provide some lessons, for example the use of Feed in Tariffs or Feed in Premiums that guarantee a long-term price for electricity from renewable generators. However, in electricity the commodity produced has a ready market and take-away system whereas with hydrogen the market does not yet exist so the commercial model needs to take account of the fact that a whole value chain from demand, supply and transportation will need to be developed. This is further complicated with blue hydrogen where you also need to factor in CO2 capture, transportation and storage.

The opportunity to learn from the mistakes and successes of others should not be missed

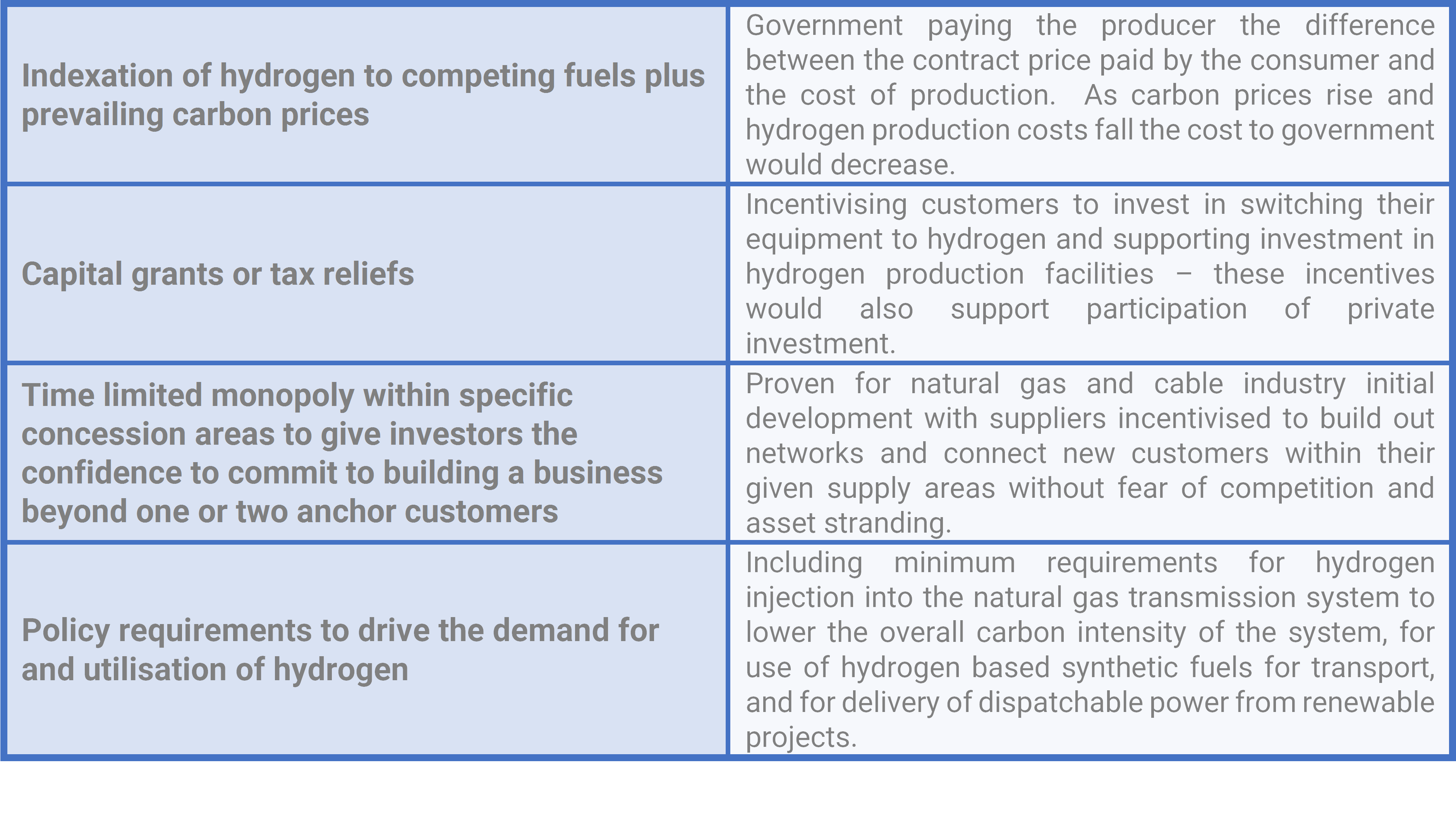

Models used for the establishment of the gas industry may again be more relevant to the development of hydrogen than those used for renewable electricity. Having established base industrial hubs and hydrogen manufacturing facilities, and underwritten initial investment, these may support confidence in wider industry conversion and local distribution enabled by incentives.

Examples of potential incentives for wider hydrogen adoption

Whatever the technical attraction of hydrogen, the imperative must be to address the commercial realities of attracting investment and adoption-in-use if it is to play a significant role in the drive to decarbonise energy economies globally. Government can provide support, but it depends on industry to pull it across the line. Providers of capital as equity and debt will play a significant role in this shift, but the early opportunities and leverage may come in smaller niche opportunities that fall below the value thresholds of the financial investors that are most capable of taking the inherent risks. It is encouraging to see the emerging partnerships of larger investment players providing backing to the smaller more “development” focused operators and investors as a way of securing active participation in this budding sector.

Whatever the technical attraction of hydrogen, the imperative must be to address the commercial realities of attracting investment and adoption-in-use if it is to play a significant role in the drive to decarbonise energy economies globally. Government can provide support, but it depends on industry to pull it across the line. Providers of capital as equity and debt will play a significant role in this shift, but the early opportunities and leverage may come in smaller niche opportunities that fall below the value thresholds of the financial investors that are most capable of taking the inherent risks. It is encouraging to see the emerging partnerships of larger investment players providing backing to the smaller more “development” focused operators and investors as a way of securing active participation in this budding sector.

***

Gas Strategies has been working closely with its clients to help them explore where the real business opportunities within the hydrogen economy lie, in addition to supporting them in maximising value from their existing natural gas and LNG businesses in the face of global decarbonisation. If you would like to find out more, and discuss how Gas Strategies can support your business today, please contact us.