Unheralded pricing dynamics

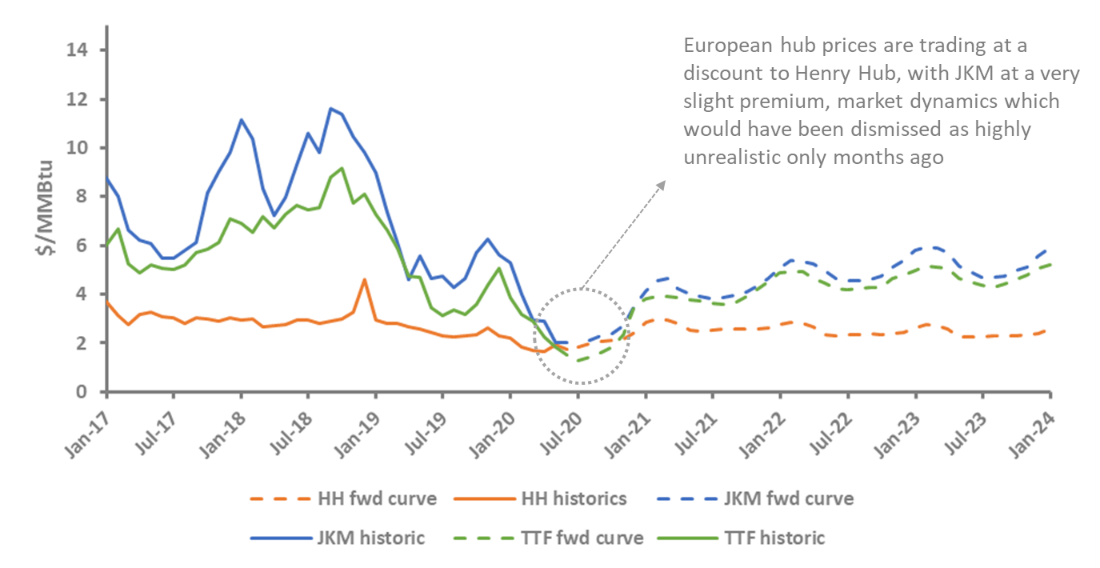

European gas prices have suffered further routs over the past week as oversupply, limited demand response and storage limitations continue to wreak havoc on markets. At the time of writing, European hub prices are well below Henry Hub with Asian LNG prices trading at a miniscule premium to US prices. As recently as last year, this dynamic may have been viewed as extremely improbable, but not only are market participants living in this reality, it seems as if this situation is here to stay for the at least the remainder of the year and potentially longer.

Figure 1 – Convergence of European, Asian and US hub prices

Source: Gas Strategies, Reuters

Source: Gas Strategies, Reuters

New mechanisms for market balancing

Times of oversupply are nothing new for LNG with investment in liquefaction capacity showing cyclical tendencies, as periods of over and under investment have led to alternating times of rapid and stagnant growth of the market. However, in the past the market has always balanced for three principal reasons: the majority of volumes sold by projects were underpinned by long-term contracts with end-market third parties, the growth trajectory of the LNG market consistently exceeded expectations, and, as last resort, liquidity of gas hubs in north west Europe allowed participants to ‘sink’ cargoes.

In the current reality of abundant supply and considerable volume length sitting on the books of portfolio players, not all production has a pre-determined ‘end market’ and European markets in their saturated state have struggled to economically absorb all excess volumes. With this failing to balance the market, current pricing dynamics have caused supply to be effectively shut-in on projects with the highest short-run marginal costs. This phenomenon is particularly impacting US liquefaction facilities where the offtake model enables buyers to “cancel” cargoes. This buyer-enforced supply side response to the global glut of LNG will help alleviate oversupply but the scale of losses facing those forced to cancel cargoes is enormous, with the reported 45 cargoes cancelled in July 2020 equivalent to a total capacity payment of approximately $500 million[1].

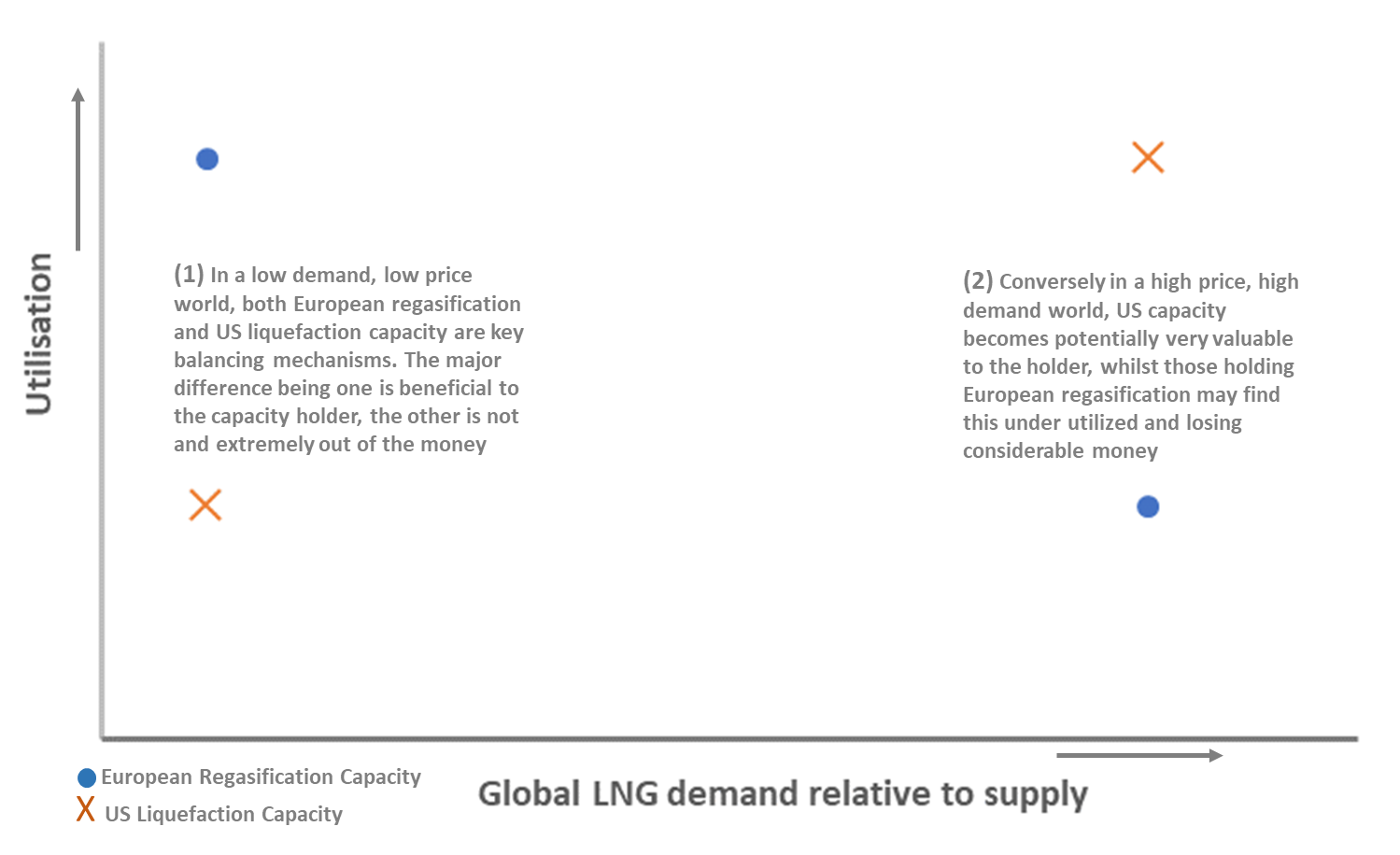

When considering the market balancing mechanisms described above, a key difference between market balancing via European markets versus an enforced supply side response is the reward to the capacity holder. US offtakers have effectively found themselves holding extremely expensive call options.

Figure 2 – The value paradox of LNG balancing mechanisms

Source: Gas Strategies

Source: Gas Strategies

Searching for signs of demand recovery

As there is still incredible uncertainty around the trajectory of future demand, the required scale and duration of these shut-ins is up for debate. What is clear is that without a marked increase in demand from key markets in Asia, decisions not to lift cargos - from US liquefaction capacity and other available mechanisms - will be a mainstay for the LNG industry for the remainder of 2020. There may be some reasons to be optimistic:

- China appears to have already suffered its dip in demand over January and February 2020, and is now importing record volumes of LNG, with volumes imported so far over Q2 up 30% versus Q2 2019.

- Government policy in South Korea in the past has pushed coal-to-gas switching to tackle environmental issues. A blocker to this has been the economics of doing so, however with oil linked LNG import prices now being competitive versus Australian coal imports, there is both political, environmental and economic rationale to increase CCGT use at the expense of coal. The last time the country had a sustained period of coal-to-gas switching was in 2018 where LNG imports ended up at a record 45 mt. If imports follow this pattern in 2020, this would represent 12.5% YoY growth in demand.

- Low prices appear to be stimulating demand across price sensitive regions, with India seeing surging imports in Q1 before the nation went into lockdown (and LNG demand plummeted as a result), both Bangladesh (+20%) and Thailand (+11%) are also seeing strong YoY increases in demand.

Whilst optimistic signs will be appreciated by an industry facing waves of bad news in 2020, progress is ultimately dependent on the future recovery of economies in the post-COVID-19 world.

Managing US capacity in the here and now

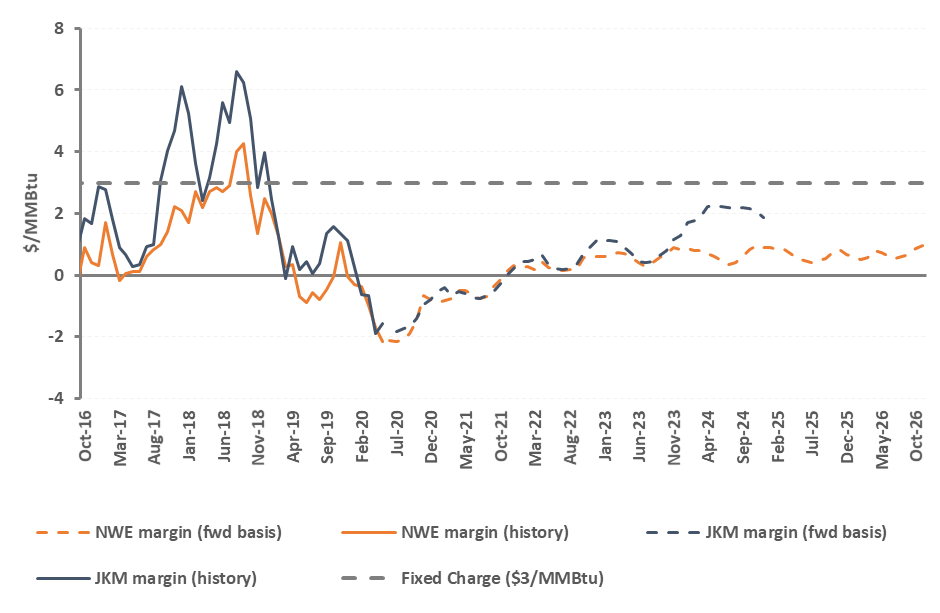

Despite some signs of potential demand recovery, cancellations look likely until summer 2021 at a minimum based on spot prices and forward curves at their current levels.

Figure 3 - Variable margin vs. fixed charge for US contracts

Source: Gas Strategies, Reuters

Source: Gas Strategies, Reuters

Of course, prices may rebound with seasonal demand over the winter season, but this is still months away. What if we have entered a world where, during sustained periods of oversupply such as we are seeing at present, prices dictate that cargo cancellations from the US become the norm and lifting cargoes the exception? US LNG tollers and buyers may be left holding an extremely expensive de facto market balancing mechanism which was never planned to be the case. This leads to important considerations for LNG market participants:

- How does this change the ongoing management of US contracts, both on a standalone basis and in the context of a wider portfolio?

- Is a mindset change necessary to view US capacity as a viable option only in a high demand, high price market? What does this mean for the future appetite of companies to commit to HH+ US LNG now that the reality of potentially large capacity payment losses has been seen?

- Would this view, at least in the short-term, require a change in approach to hedging and risk management? A traditional US hedging approach has been to buy Henry Hub and sell Brent. However, as JKM and LNG spot prices in general continue to decouple from oil, is this the correct approach?

- Many US offtakers chartered vessels on a long-term basis to lift FOB volumes – what now to do with this shipping length? Do organisations have the capability to monetise vessels via the spot market, and does the reward exist to do so?

[1] Assuming average 4TBtu per cargo at a capacity payment of $2.75/MMBtu

For an example of our work in providing commercial due diligence on an operational US LNG project please click here.

***

If you would like more information about how Gas Strategies can help your business with Consulting services across the value chain or provide industry insight with regular news, features and analysis through Information Services or help with people development through Training Services, please contact us directly.