With just over a month to go before the end of meteorological winter in the northern hemisphere – a definition of winter which tends to reflect seasonal temperatures better than the astronomical one – natural gas prices continued their streak of price falls in Asian, European and US markets on Thursday.

Henry Hub in the US, which saw a brief intra-day dip below USD 3/MMBtu on Wednesday, closed firmly in sub-USD 3 territory, at one point reaching its lowest level since April 2021 (see separate story in today’s issue), with mild weather a key factor.

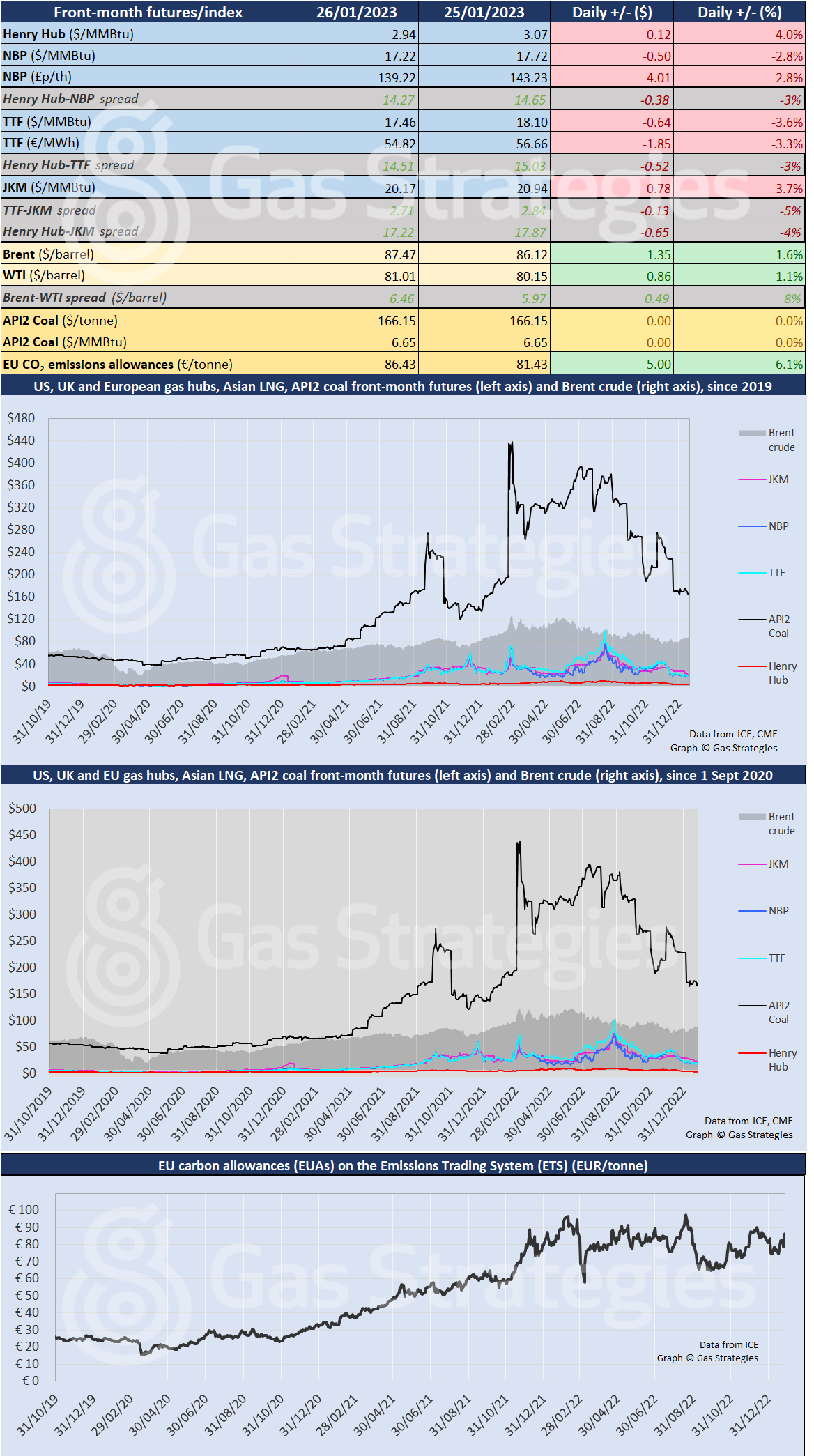

The front-month contract fell another 4.0%, from USD 3.07/MMBtu to USD 2.94/MMBtu.

In Europe, the Dutch TTF marker fell another 3.3% from EUR 56.66/MWh (USD 18.10/MMBtu) to EUR 54.82/MWh (USD 17.46/MMBtu), following the 2.8% fall the previous day, the 11.7% fall on Tuesday and the 1.3% fall on Monday. Thursday’s close was the lowest in 16 months. Overall TTF was down 18% on last week’s close, with a further fall expected on Friday.

Milder weather was again a driving factor along with expectations of greater availability of US LNG as Freeport moves towards resuming production, with the US Federal Energy Regulatory Commission yesterday confirming its approval for re-start operations to begin. There are reports that gas has begun to flow into the plant.

In what is still a tight market by historical norms, another 15 mtpa of destination-flexible LNG will make a big difference – in both Europe and Asia – at least until China’s LNG imports recover from last year’s collapse.

The UK’s NBP was down 2.8% from 143.23 p/therm (USD 17.72/MMBtu) to 139.22 p/therm (USD 17.22/MMBtu).

The JKM Asian LNG marker fell by 3.7% from USD 20.94/MMBtu to USD 20.17/MMBtu, remaining USD 2.71/MMBtu above TTF in dollar terms despite a 5% fall in the TTF-JKM spread. The differential is partly explained by high storage levels in Europe, reducing the need to pull LNG cargoes away from Asian markets.

Crude prices were up, with Brent rising 1.6% from USD 86.12/barrel to USD 87.47/barrel and WTI rising 1.1% from USD 80.15/barrel to 81.01/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.

Related Stories

-

26Jan2023

26Jan2023Pricewatch | 26 Jan 2023 | Gas Matters Today

25Jan2023

25Jan2023Pricewatch | 25 Jan 2023 | Gas Matters Today

24Jan2023

24Jan2023Pricewatch | 24 Jan 2023 | Gas Matters Today