- LNG shipped in 2019 contributed some 325 million tonnes of CO2 equivalent

- Buyers showing increasing interest in emissions profile of LNG they’re buying

- Sellers beginning to view emissions footprint as a source of competitive advantage

- Clearer system of benchmarks or certification required for emissions profiling

While the Covid-19 pandemic and its effects continue to dominate the news in 2020, a critical development has been playing in the background: the acceleration of policy responses to climate change. The most important was China’s announcement in September that it aims to achieve carbon neutrality “before 2060”. IOCs have also set targets to reduce and eventually eliminate the emissions from their operations.

These targets are bound to have an impact on the LNG business, with an increasing emphasis on the carbon emissions of the oil and gas industry itself. As a result, the LNG industry will have to provide a more sophisticated response to the decarbonisation agenda than relying on arguments about gas being ‘the cleanest fossil fuel’ and the benefits of displacing coal.

Coming after the first deals for ‘carbon neutral’ LNG cargoes in 2019, Pavilion’s buy side tender in April this year reflected the increasing interest buyers are showing in the emissions profile of the LNG they buy. There are now signs of producers viewing their emissions footprint as a source of competitive advantage, most recently with NextDecade announcing a plan to add a Carbon Capture and Storage (CCS) stage to its Rio Grande project.

While interest in this area has grown hugely, there is little information available to compare projects and no generally accepted methodologies or rankings that look at emissions along the whole LNG chain. In the first of a series of articles on greenhouse gas (GHG) emissions, LNG Business Review looks at how much emissions the LNG industry does in fact generate and what it can do about it.

Production coming under scrutiny

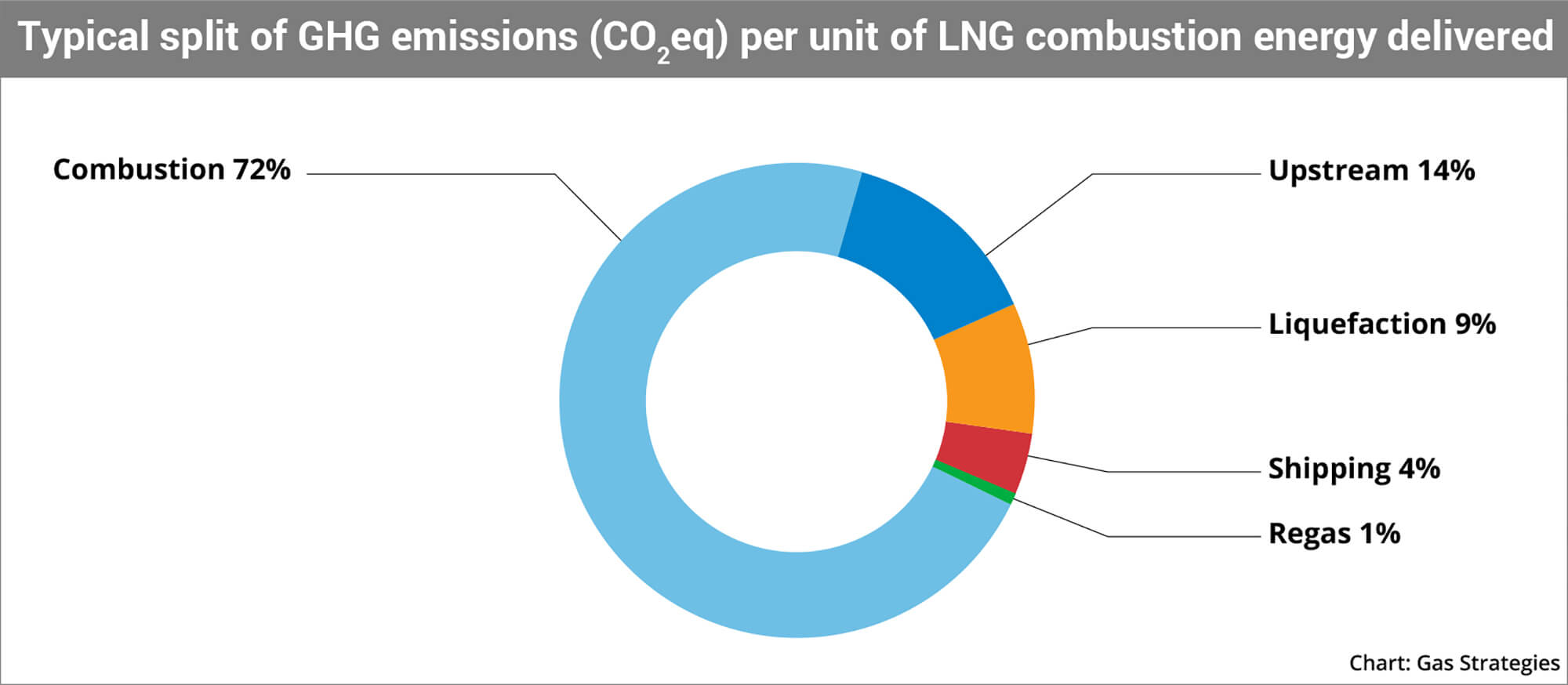

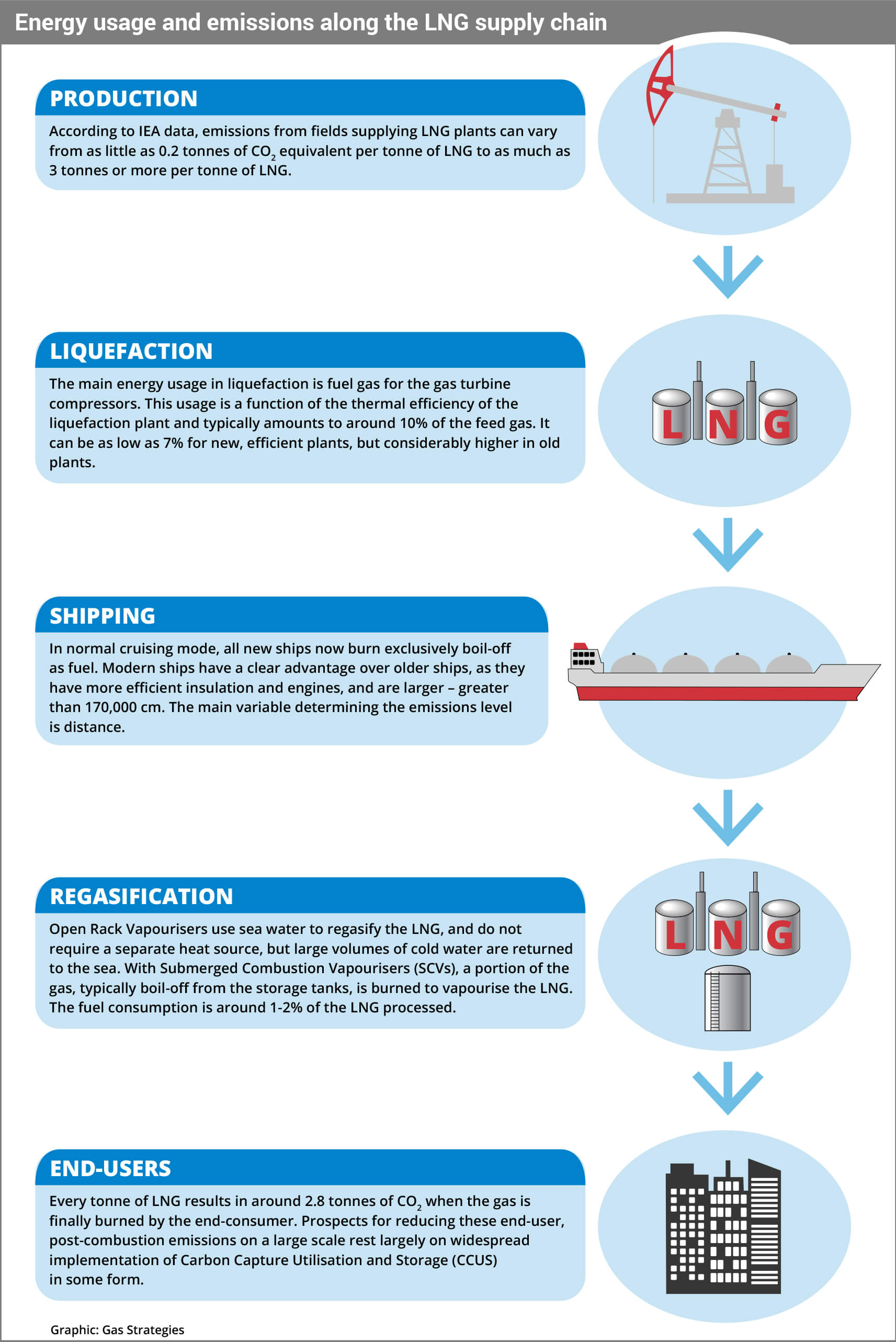

Every tonne of LNG results in around 2.8 tonnes of CO2 when the gas is finally burned by the end-consumer. Prospects for reducing these end-user, post-combustion emissions on a large scale rest largely on widespread implementation of Carbon Capture Utilisation and Storage (CCUS) in some form. While ‘carbon neutral’ cargoes such as those Shell sold to GS Energy and Tokyo Gas last year, and to CPC and CNOOC this year, captured headlines, achievement of carbon neutrality in these cases relies on offsetting emissions through purchasing emissions certificates or investing in environmental projects.

While it may be possible, at a price, to offset the emissions from a few cargoes – and some buyers may be prepared to pay a premium for this – there is no realistic chance of offsetting any major part of the global LNG production.

Emissions from the end-use of LNG are not the whole story. Pre-combustion emissions from gas production, liquefaction, shipping and regasification are significant. This is at the basis of claims that, when these emissions are taken into account, LNG’s carbon footprint is no better than coal. While such claims are demonstrably false, the level of pre-combustion emissions, including methane emissions from the upstream, is substantial, amounting on average to around a third of the emissions produced when the LNG is finally burned – albeit with, as discussed below, very significant variation.

This means that the production, shipping and regasification of the 355 million tonnes of LNG shipped in 2019 contributed some 325 million tonnes of CO2 equivalent – somewhere between the total emissions of France (299 mt CO2e) and those of the UK (387 mt CO2e).

With this level of emissions, there is no doubt that there is going to be more and more scrutiny of the emissions profile of LNG projects. Buyers and financiers are increasingly going to be asking how the emissions profile of one project compares with that of another.

The five-year 2 mtpa tender launched by Pavilion in April was the first to include the idea that emissions might be a factor in the award of a supply contract. The tender requested ideas from suppliers for GHG emission reduction and also suggested collaboration on developing methodologies for benchmarking emissions, highlighting the fact that, although emissions from LNG production and transport are coming under scrutiny, there is no uniform methodology for comparing projects.

While there currently are no industry-wide benchmarks, it is clear that there are some sizeable differences between projects, with variations in the emissions profile all along the LNG chain.

Energy-consuming processes

Emissions start at the level of gas production and come from various sources. But there are two upstream emissions sources that stand out and are the greatest source of variation: vented CO2 and methane emissions. Differences in emissions from these two sources are the main reason why, according to International Energy Agency (IEA) data, emissions from fields supplying LNG plants can vary from as little as 0.2 tonnes of CO2 equivalent per tonne of LNG to as much as 3 tonnes or more per tonne of LNG.

Many gas streams contain substantial amounts of CO2 and this has to be removed before the gas is liquefied. Standard industry practice is to vent this CO2, which obviously adds directly to the emissions profile. It is possible, at least in some circumstances, to reinject the separated CO2 and essentially eliminate these emissions. This is done on both the Snohvit and Gorgon LNG projects, where the fields contain around 5% and 15% CO2 respectively.

Methane emissions are the other major – and controversial – source of upstream emissions. They are caused by gas escaping during various aspects of the production process, with hydraulic fracturing being blamed as the biggest offender in this area. But methane escapes are difficult to measure and the exact levels of emissions are uncertain.

While methane is a much more potent greenhouse gas than CO2, it is much less long-lasting in the atmosphere, and so the impact in terms of CO2 equivalents depends on the timescale over which the emissions are considered. Despite these issues, the fact is that upstream methane emissions can largely be eliminated with the right design of processes, and most of the oil and gas majors have made some commitment to reducing methane emissions.

Downstream from the gas production, liquefaction is the next significant emissions source – though if the fields are far from the liquefaction plant, requiring a long-distance pipeline, there may be compressor gas usage or pipeline leakage to take into account.

Liquefaction is inherently energy consuming and in most plants the main energy usage is fuel gas for the gas turbine compressors. This usage is a function of the thermal efficiency of the liquefaction plant and typically amounts to around 10% of the feed gas. It can be as low as 7% for new, efficient plants, but considerably higher in old plants.

From liquefaction to regas

There are theoretical limits on what can be done to improve liquefaction efficiency. Nevertheless, there are some ways in which the liquefaction plant emissions can be substantially reduced. The subject of liquefaction plant emissions is receiving close attention, with Siemens and Total, for example, announcing in June that they were working together on new concepts for low-emission LNG production. But other than tweaking the process, there are two potential ways to drastically reduce emissions from the liquefaction plant.

The first is to use electrical drives on the compressors instead of gas turbines. This allows the compressors to use electricity which is wholly or partly generated from low-carbon sources. Currently, the Snohvit plant in Norway and the Freeport facility in the US are the only existing plants with electrical drives. In theory it would be possible to retro-fit electric drives to conventional plants, but the economics of this would depend on the value of emission reductions – which is a whole subject in itself.

The other way to reduce emissions from the liquefaction plant would be to capture and store the CO2 from the liquefaction plant, as opposed to, or in addition, to the CO2 separated from the feed gas. This seems to have been the basis of the announcement made by NextDecade earlier this month that it is looking at CCUS as a means of reducing emissions from the proposed Rio Grande project by up to 90%.

CCUS is a burgeoning area in the US, which has a plethora of depleted fields that can potentially be used, as well as a limited network of CO2 pipelines and a favourable regulatory environment. However, CCUS is a major additional investment and, as with conversions to electric drives, the economics are difficult to assess.

Downstream of the liquefaction plant, the main source of emissions is in shipping, with all new ships now burning exclusively boil off as fuel – at least in normal cruising mode. Modern ships have a clear advantage over older ships, as they have more efficient insulation and engines, and are larger – greater than 170,000 cm.

A lot of progress has been made in recent years in improving ship efficiency, and Shell has estimated that ships currently on order will have 60% lower emissions than a steam-turbine ship from the early 2000s. But the main variable determining the emissions level is still distance. Around 5% of the cargo is consumed as fuel for a delivery from the US Gulf Coast to Tokyo via the Panama Canal, whereas the consumption is only half that for a cargo originating in Australia. While efficiency improvements will continue to be made, it is difficult to see major further inroads being made into the emissions from LNG shipping.

Finally, at the end of the LNG chain, there are the emissions resulting from the process of regasification. Open Rack Vapourisers, which are the most common technology employed in regasification terminals, use sea water to regasify the LNG, and do not require a separate heat source, but have their own environmental problems because of the large volumes of cold water returned to the sea. The next most commonly-used regasification technology is Submerged Combustion Vapourisers (SCVs), where a portion of the gas, typically boil-off from the storage tanks, is burned to vapourise the LNG. The fuel consumption is around 1-2% of the LNG processed.

Ambient air vapourisers have also been tried, and require essentially no external power source, other than for pumping the LNG, but do not have the SCV’s ability to rapidly ramp up regasification to high volume flows.

Tailoring buyer practices

This survey of the sources of emissions along the LNG chain suggests that there is likely to be very significant variation in the emissions profiles of different LNG projects. In the absence of any agreed methodologies or benchmarks it is difficult to make comparisons. However, it is clear that projects which have high levels of CO2 venting and/or methane emissions could easily have total emissions intensities which are multiples of the lowest emitting projects.

A report commissioned by Woodside and published in April this year compared full chain emissions intensity for the proposed Scarborough and Browse projects. It concluded that the Browse emissions would be around twice those of Scarborough, principally due to vented CO2 and greater offshore processing requirements.

A paper published in the scientific journal Nature in February compared emissions intensities of different gas supply sources for China, concluding that Qatar was the LNG supply source with the lowest emissions intensity at 3.9 kg CO2e/GJ while the US had the highest emissions intensity at 19.7 kg CO2e/GJ. At the same time, the research indicated that pipeline supply to China had a higher emissions intensity than LNG, with methane leakage from pipelines having a major impact.

Another conclusion that can be drawn is that there is quite a lot that can be done to reduce emissions. For example, in the US where, as the Nature research shows, upstream emissions are a significant issue, liquefaction projects, or their capacity holders, can tailor their buying practices to favour suppliers that have low emissions profiles and/or have programmes in place to reduce emissions. This could actually lead to LNG being a force for change in reducing the emissions intensity of the US upstream.

However, some of the ways of reducing emissions – such as CCUS – will require some substantial investment, while others – such as electric compressor drives – may not be an option for existing plants. For projects to make substantial investments in order to reduce the emissions intensity of their production they will need a clear idea of how much it is worth to have a lower emissions intensity than their competitors.

In the here and now there does not seem to be a significant price advantage in having a lower emissions profile, but in a paper published in October 2019, Jonathan Stern of the Oxford Institute of Energy Studies (OIES) argued that LNG suppliers with higher emissions, or who cannot certify their emissions levels, “run the risk of progressively being deemed to have a lower commercial value”. This is because they will require buyers to purchase emission offsets of various types, eventually being excluded from jurisdictions with the strictest standards.

How soon Stern’s vision of emissions intensity being a key source of competitive advantage or disadvantage may come true is uncertain. Will it at some point begin to impact existing long-term contracts? Will it effectively become another way for sellers to potentially generate revenue by trading their carbon credits in the short term? Looking forward, a key step will need to be some clearer system of benchmarks or certification. But, with the focus on emissions from buyers and financiers ramping up, the topic is pushing itself forcefully on to the agenda of all suppliers. - DD

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.