- Pavilion Energy closing in on world’s first term deal for carbon-neutral LNG

- Framework needed for monitoring, reporting and verifying (MRV) emissions

- Carbon-neutral LNG offering could give producers a competitive edge

- Low prices and oversupply may help drive demand for carbon-neutral LNG

Pavilion Energy is closing in on the world’s first term supply deal for carbon-neutral LNG after issuing a request for proposal (RFP) in April. As part of the RFP, the firm requested potential suppliers to commit to jointly develop and implement a greenhouse gas (GHG) quantification and reporting methodology, covering emissions from the wellhead through to the LNG terminal.

Spinning the line of ‘gas being the cleanest burning fossil fuel’ is no longer enough for the industry facing the decarbonisation agenda, as emphasis of regulators and public opinion has shifted to GHG emissions associated with the LNG full value chain. LNG Business Review examines whether trade of carbon-neutral LNG will become the norm as the decarbonisation agenda grips the globe and how the LNG sector will look to mitigate emissions.

‘Stay competitive’

To date, trade of carbon-neutral LNG has been centred on Asia, with deals limited to spot transactions.

June 2019 saw Shell announce the sale of the world’s first carbon-neutral LNG cargoes to Tokyo Gas and South Korea’s GS Energy. Hot on the heels of Shell’s announcement, JERA confirmed the sale of its first spot cargo with carbon offsets to a buyer in India.

Shell followed up last years’ deals with a pair of spot sales this year with Taiwan’s CPC and China’s CNOOC.

However, with Singapore-based Pavilion Energy’s RFP seeking ‘green LNG’, the company has signalled buyers interest in procuring long-term carbon-neutral LNG supplies, and the company is also looking to play a key role in helping set an industry standard for GHG quantification.

What is carbon-neutral LNG?

LNG sold as carbon-neutral still causes GHG emissions, however the parties involved in the trade of the cargo agree to buy carbon credits for the equivalent amount of GHG emissions associated with the cargo.

The credits are associated with carbon removal projects such as reforestation, afforestation or renewable projects.

GHG emissions generated from the entire value chain are considered (scope 1, 2 and 3 emissions) when offsetting LNG cargoes.

For a cargo to typically be classed carbon-neutral, the entire product lifecycle GHG emissions (from well to wheel) are offset.

The cargoes sold by Shell to Tokyo Gas, GS Energy and CPC, covered Scope 1, 2 and 3 emissions in the carbon offset calculation. The cargo sold by JERA – sourced from ADNOC – saw emissions offset from the downstream use of the LNG.

“We encourage bidders to tell us what they are doing to reduce their emissions. The methodology needs to be accurate and verifiable based on international standards…and with a transparent approach with defensible data for each LNG cargo,” Pavilion Energy’s CEO Frederic Barnaud said in April.

“Pavilion foresees a reality where carbon-neutral LNG will be a requirement to stay competitive where industries eventually evolve to a state where carbon neutrality becomes a norm for us all,” added Barnaud.

The tender is for 2 mtpa under a five-year term starting in 2023, with Pavilion looking to place the majority of the volume into Singapore, Barnaud said. However, Pavilion’s CEO said volumes could be made available across its portfolio, including Europe.

Demand drivers

Market observers agree that there are several factors driving trade of carbon-neutral LNG, with the majority pointing to end users and their wanting to comply with climate goals as the main driver.

“There are multiple drivers but they play out in different ways. Consumers care, governments care, companies care, and again, in every jurisdiction you will see a different leader pushing it,” Randolph Bell, director of the Atlantic Council’s Global Energy Center (GEC) tells LNG Business Review.

“All matter because you have to have the ability to produce the carbon-neutral LNG, so you have to have companies on the supply side willing to create that – that will come from shareholders that are pushing these companies to have their products be more climate-friendly. On the demand side, you have to have government and buyers who care as well,” adds Bell.

Erin Blanton, senior research scholar at the Center on Global Energy Policy at Columbia University, agrees that end users are key in the drive of carbon-neutral LNG trading. However, she suggests the finer details need to be worked out in order for trade to expand.

“There is an interest from end users to see a differentiation of gas products but they don't really know what premium they would be willing to pay for reduced carbon LNG because they don't have a good sense of what the costs would be to producers,” says Blanton.

“Even the GHG offset cargoes to date appear to have been the product of long negotiations between the buyer and seller. There also has to be clarity on who bears the cost of the carbon offset? If it is the buyers of the LNG, then they want assurance that they could pass that premium on to end users, for example getting approval from regulatory agencies. That said there is definitely a growing interest for this market to develop as buyers try to comply with sustainability goals,” adds Blanton.

Pavilion’s want for carbon-neutral LNG shows buyers are starting to profile the emissions of suppliers – something Professor Jonathan Stern at the Oxford Institute for Energy Studies (OIES) expects to become more mainstream, with regulatory changes driving buyers approach to deals.

“I would say it [emissions profiling] is definite – particularly in Europe – and this will be driven by action on carbon/methane prices/taxes relative to an emission standard,” Stern tells LNG Business Review.

"The EU methane strategy will be published next month and we expect more detail on this. I am currently writing a new paper which anticipates that in Europe (and potentially elsewhere) inability to produce methane/GHG emission certificates will impact the value of cargoes,” adds Stern.

Framework needed

Market observers agree more needs to be done to verify GHG emissions – not just for offsetting but also for reducing emissions directly across the value chain.

“The basic requirement, before we get to permits, will be verified and certified emissions using completely transparent measurement methodologies,” says Stern.

A universally accepted framework for monitoring, reporting and verifying (MRV) emissions would be “ideal” according to Stern, however the first step must be to “define a measurement and reporting regime – bottom-up and top-down reconciliation – which defines how these must be carried out, and then reported, in relation to different parts of the value chain.”

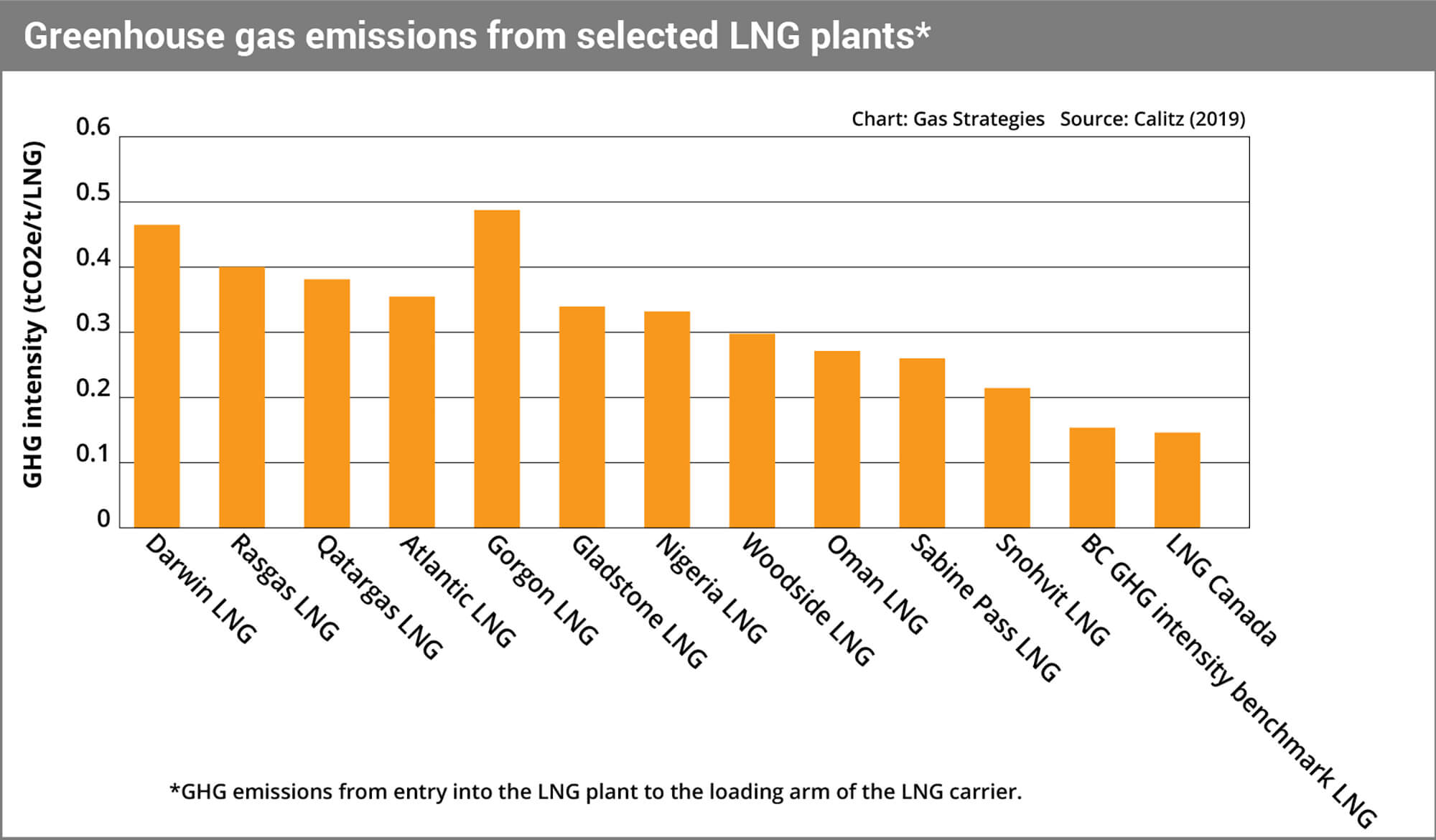

Without a universal MRV framework, it is difficult to verify and quantify emissions related to LNG cargoes, with emissions profiles differing depending on the source of the LNG, the LNG carrier and the liquefaction and regasification technology. However, UK government GHG conversion factors suggest ~75% of GHG emissions from LNG are derived from downstream consumption.

Whilst a universal MRV framework would be the “ideal”, climate targets in different jurisdictions may hamper the formulation of a central framework.

“The problem around a universally accepted framework is that takes time. It could be that there will develop more than one framework, which is also fine as long as those frameworks each are deemed to provide reliability and accuracy,” says Jonathan Elkind senior research scholar at the Center on Global Energy Policy.

“I don’t think it necessarily needs to be a singular framework but the criteria that are important are the reliability and accuracy of the framework,” adds Elkind.

Whilst carbon credits are a first step to decarbonising the LNG sector, they fail to address the direct production of GHG emissions. Sources agree that offsets will largely act as a bridge in the LNG sector’s decarbonisation push.

“The offset option could serve as a temporary way to lower the carbon footprint of LNG cargoes. But the most obvious and effective way to decarbonise the LNG sector is to reduce and avoid methane and CO2 emissions along the LNG value chain,” says Blanton.

Shell agrees that avoiding emissions should be the priority.

“Our strategy is to first avoid emissions where we can, and reduce them. Offsetting is only for unavoidable emissions,” Mehdi Chennoufi, General Manager LNG Origination and Business Development at Shell tells LNG Business Review.

One market source tells LNG Business Review “we need to be realistic about the extent to which offsetting can deliver at the scale of the total energy system.”

“As an order of magnitude it looks like a massive global reforestation program would at best be able to offset somewhere in the range 1-5 Gt of CO2/year. A large number, but only a small percentage of the current 35 Gt/year global emissions,” the source says.

Competitive edge

With key stakeholders pushing for greater transparency on GHG emissions, LNG sellers and project developers are starting to take heed of the decarbonisation agenda.

Notably, US LNG players have been active in drawing attention to their emission reduction efforts, with the most extreme example being the relaunch of Louisiana-based G2 LNG – now named G2 Net-Zero LNG – which is aiming to construct the world’s first net-zero carbon emissions LNG facility.

The firm exited the federal permitting process in 2017 and is now planning to restart the permitting process next year after returning to the drawing board to differentiate itself from the competition.

The proposed 13 mtpa plant aims to capture 85% of upstream and midstream emissions, with the remaining 15% offset using carbon credits, G2 Net-Zero LNG’s chairman Charles Roemer said earlier this year.

Sources largely agree that the offer of carbon-neutral LNG could give producers a competitive edge, especially in jurisdictions where GHG emissions reduction is an important part of government policy.

“You could have competitive edge in places that decide that lowering greenhouse gas emissions is a priority and that have already made that switch from coal-to-gas and are looking for further reductions,” says Bell.

“There are other parts of the more developing world where they are still making that transition from coal to gas and I don’t think it will be as relevant in the short-to-medium-term in those jurisdictions, where the coal-to-gas switch is a really big jump in itself,” adds Bell.

However, Blanton believes producers of ‘green LNG’ will not have a competitive edge until “there is accurate monitoring of producer's emissions”.

“Until that happens, there will be a lack of incentive for suppliers to make the additional investments to produce lower emission LNG and a fear of greenwashing by end users and the investment community,” says Blanton.

Perfect opportunity?

Sources are split over whether current market conditions – oversupply and low prices – make for the perfect opportunity to expand trade of carbon-neutral LNG.

Investing in reforestation projects to offset GHG emissions from LNG cargoes can see costs “easily rise to USD 10/tCO2e or more”, according to GIIGNL.

“At this cost, if one assumes the total GHG emissions of a conventional LNG cargo at around 250,000 tCO2e, offsetting GHG emissions for one LNG cargo amounts to USD 2.5 million/cargo, i.e. approximately USD 0.60/MMBtu,” according to GIIGNL estimates.

With gas prices currently trading below the USD 3/MMBtu mark, offset costs pose a significant premium, which could deter buyers facing a severe economic downturn due to the Covid-19 pandemic.

“[G]lobal gas prices are so low and gas consumption is so impacted by Covid-19 that the industry is in survival mode - it is hard for either sellers or buyers to absorb the additional cost of offsetting the carbon,” says Blanton.

“However, as the global economy starts to recover then I do think that having a well-supplied LNG market will keep prices low enough that carbon-neutral LNG could become an attractive "bridge" option for buyers and sellers,” adds Blanton.

Shell is however optimistic that current market conditions can drive the carbon-neutral LNG offering.

“The current low-price environment can encourage more buyers to look at decarbonising their energy purchase as the fuel cost component of the end product cost gets smaller and we hope that more partners will consider carbon-neutral LNG cargoes as an option,” says Chennoufi.

Others see the offering of carbon-neutral LNG in the current market as a means for suppliers to distinguish themselves in a bid to seal deals.

“I think carbon-neutral LNG supply is in its infancy and the players pushing it are keen to find a USP for their LNG. In the current market of oversupply and low prices, any distinguishing feature of ones LNG supply can only be a good thing in terms of trying to find an end market/customer,” one market expert tells LNG Business Review.

“I would imagine that at this stage, sellers of carbon-neutral LNG are leveraging their product to win business, not necessarily create a premium for their product (which could come later down the line when markets balance). I.e. if a buyer has the choice of 3 cargoes all at the same or very similar price but one is ‘carbon-neutral’, it is an easy win for them,” the expert adds.

Whilst Bell agrees that low prices may help drive demand for carbon-neutral LNG, he believes market conditions are not the most important driver.

“I think the more important driver is the attitude about addressing climate change in this environment. Europeans and the Japanese have made it very clear that the recovery will be a green recovery and that they need to take action now,” says Bell.

“This is being discussed across many capitals – that this is actually a time when you are going to need to make massive investments in clean energy. So this is really a time when there’s a question over the future of gas and the role of gas in clean energy future, that the industry can step up and actually say here’s what we can do and here’s why this is important,” concludes Bell. - ET

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.