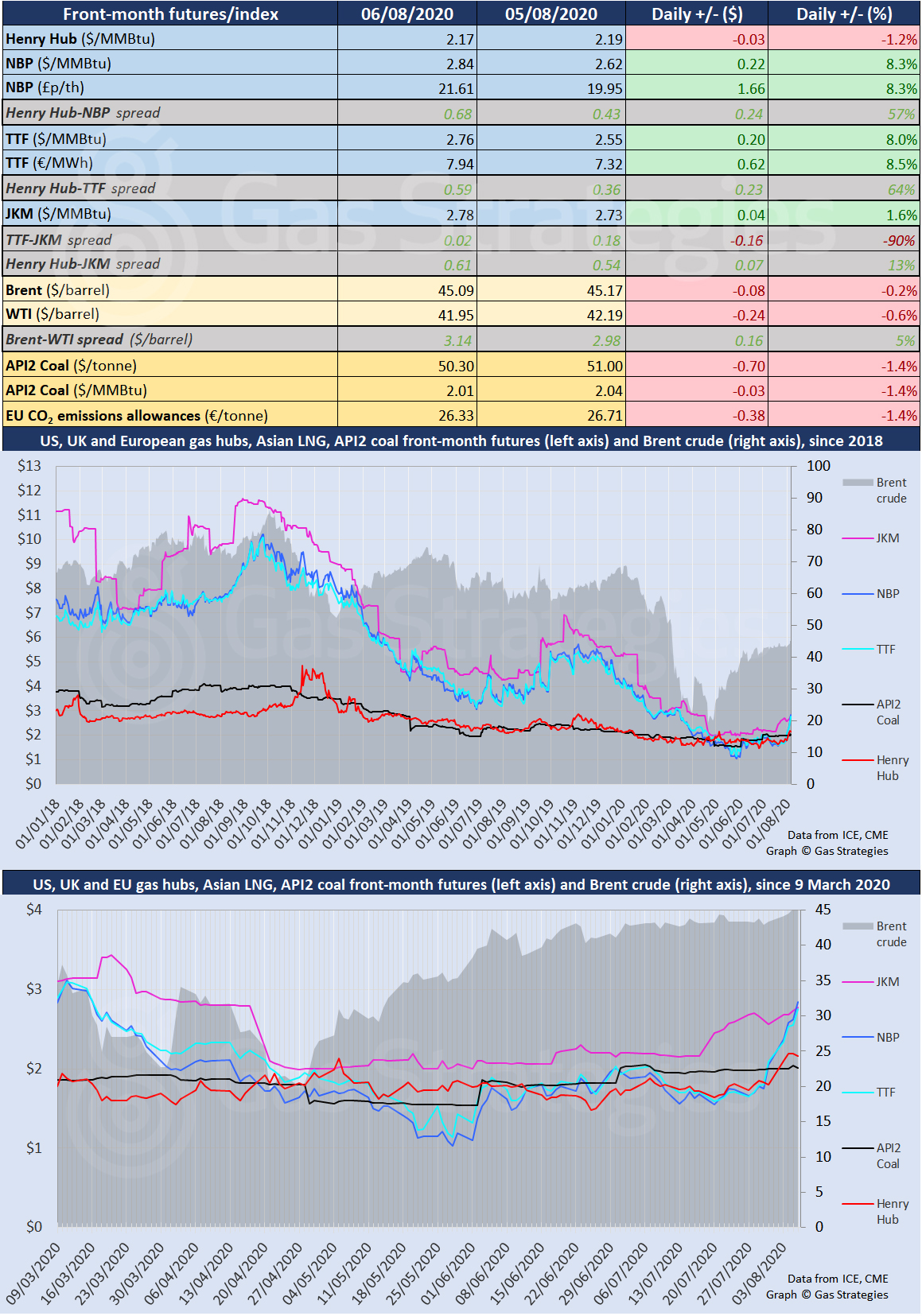

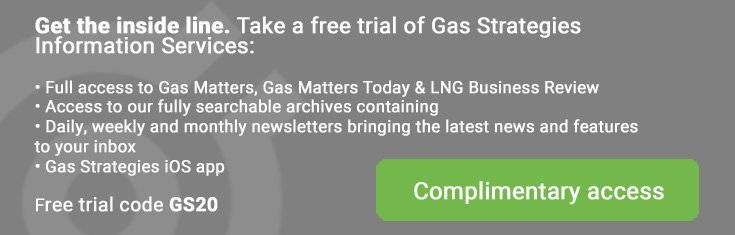

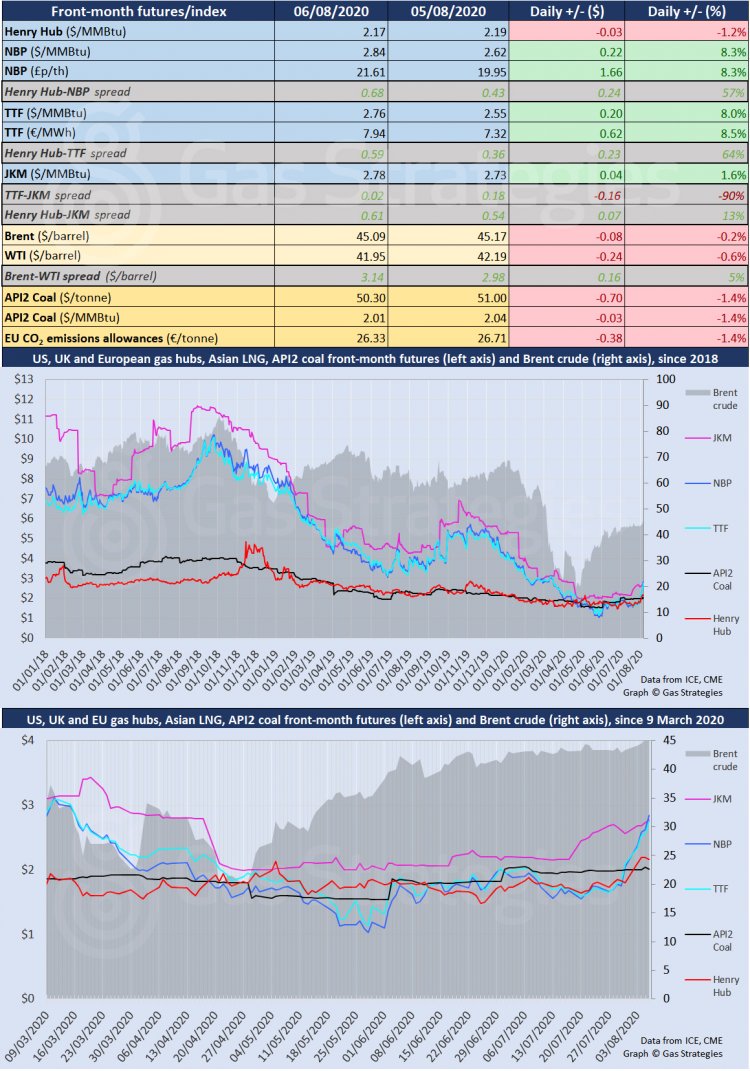

European gas hubs returned to strong growth yesterday by mounting a fresh rally that has closed the gap between the UK wholesale price and the prevailing Asian LNG spot price. Front-month UK NBP soared 8.3% to USD 2.84/MMBtu, surpassing CME’s JKM futures, which closed up 1.6% at USD 2.78/MMBtu. Dutch TTF is not far behind, having leapt 8.5% to USD 2.76/MMBtu on Thursday.

The EU/UK gas gains are being driven by a sharp uptick in Ukrainian imports that has drawn Russian gas volumes via Nord Stream away from markets lying to the west, with prompt prices in Slovakia, the Czech Republic, Hungary and Austria all reportedly commanding heavy premiums to TTF.

Unlike recent EU/UK gas rallies, this one is not driven by a surging US gas price. US benchmark Henry Hub yesterday fell 1.2% to USD 2.17/MMBtu, widening the HH-TTF spread to its USD 0.59/MMBtu – its widest since mid-April 2020.

Crude oil prices fell back slightly yesterday and opened lower on Friday, with Brent and WTI today trading almost 1% below their Thursday closing prices of USD 45.09/barrel and USD 41.95/barrel.

The European carbon price fell further in yesterday’s session, as the month-ahead futures contract for ETS carbon allowances (EUAs) lost 1.4% to close at EUR 26.33/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights reserved.