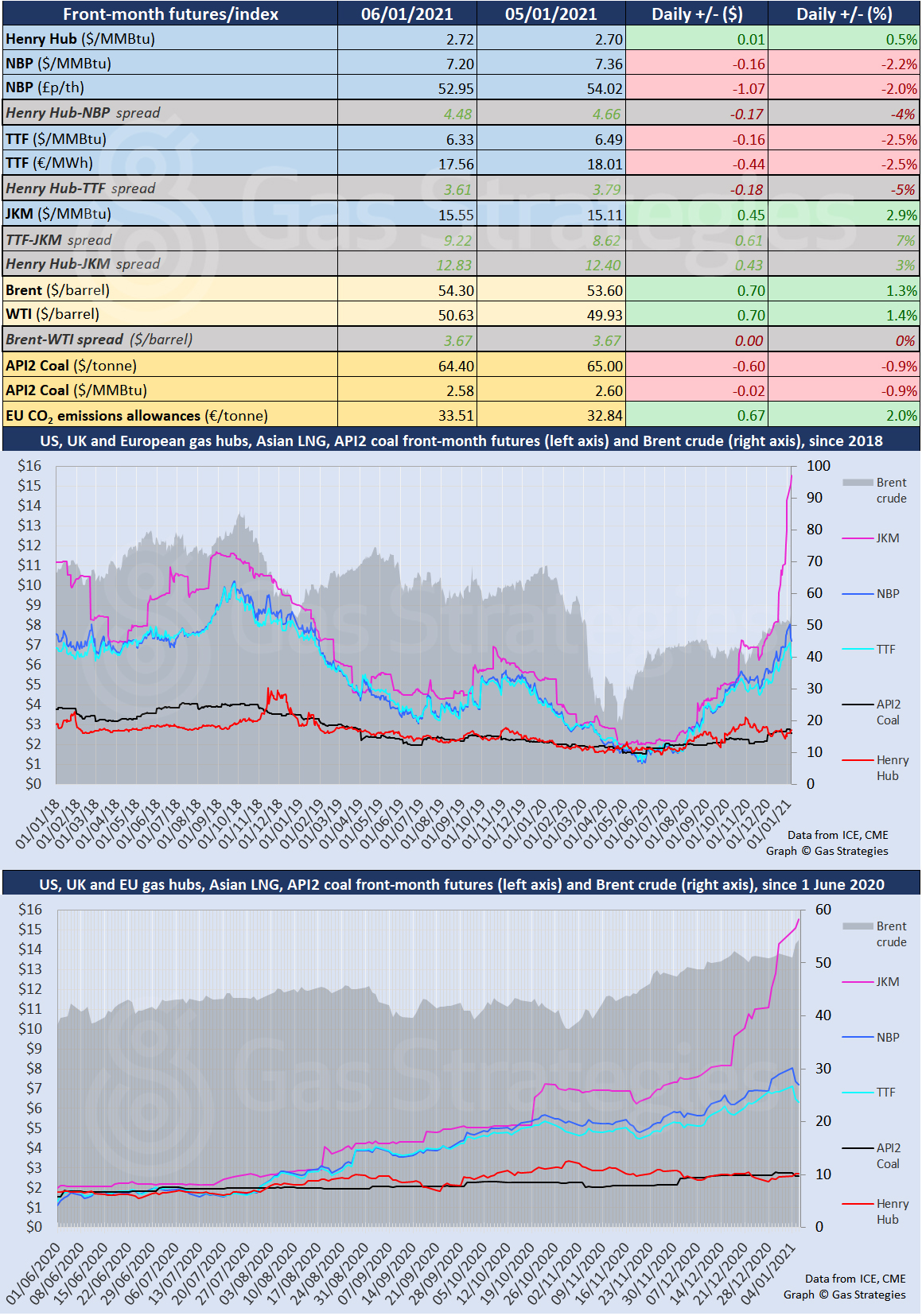

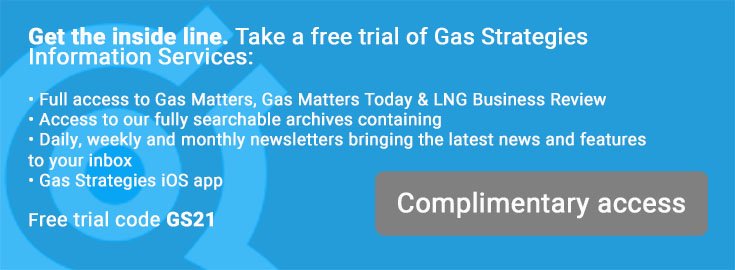

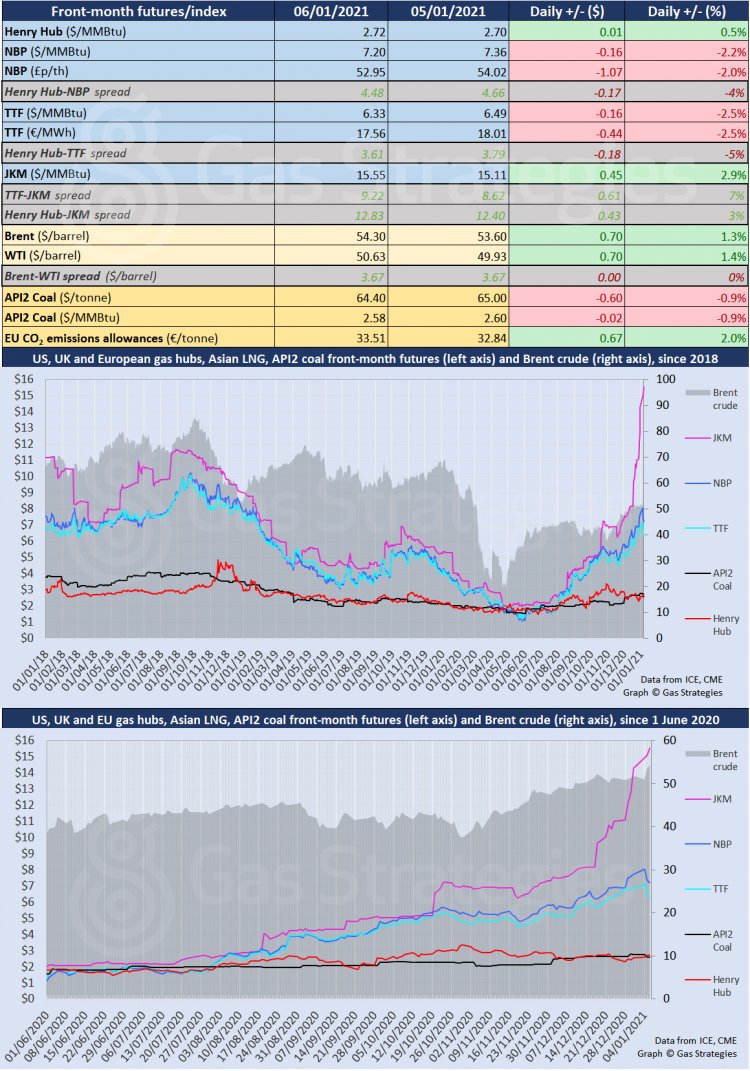

Crude oil prices continued their upward trajectory on Wednesday following Saudi Arabia’s unilateral voluntary production cut, which helped propel Brent crude to USD 54.30/barrel and WTI beyond the USD 50/barrel threshold. Meanwhile, dramatic scenes in the US of rioters invading Capitol Hill in a bid to prevent a peaceful handover of power seemed to give Brent further momentum as the uncertainty weighed on the US dollar, the world’s reserve currency which is still used to price most oil purchases.

The Asian LNG spot price continued its bull run on Wednesday, amid reports of a trading house bidding more than USD 26/MMBtu for a February cargo. CME’s JKM futures contract, a financial hedging instrument against JKM, yesterday rose another 2.9% to USD 15.55/MMBtu, believed to be its highest closing price on record.

European gas hubs continued their sharp correction on Tuesday, with month-ahead contracts on UK NBP and Dutch TTF falling by 2-2.5% to close the session at the equivalent of USD 7.20/MMBtu and USD 6.33/MMBtu, respectively.

The European carbon price recovered Tuesday’s losses, with EU ETS allowances (EUAs) gaining 2% and settle at EUR 33.51/tonne and shaping up to possibly hit a fresh all-time high in the coming days.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights reserved.