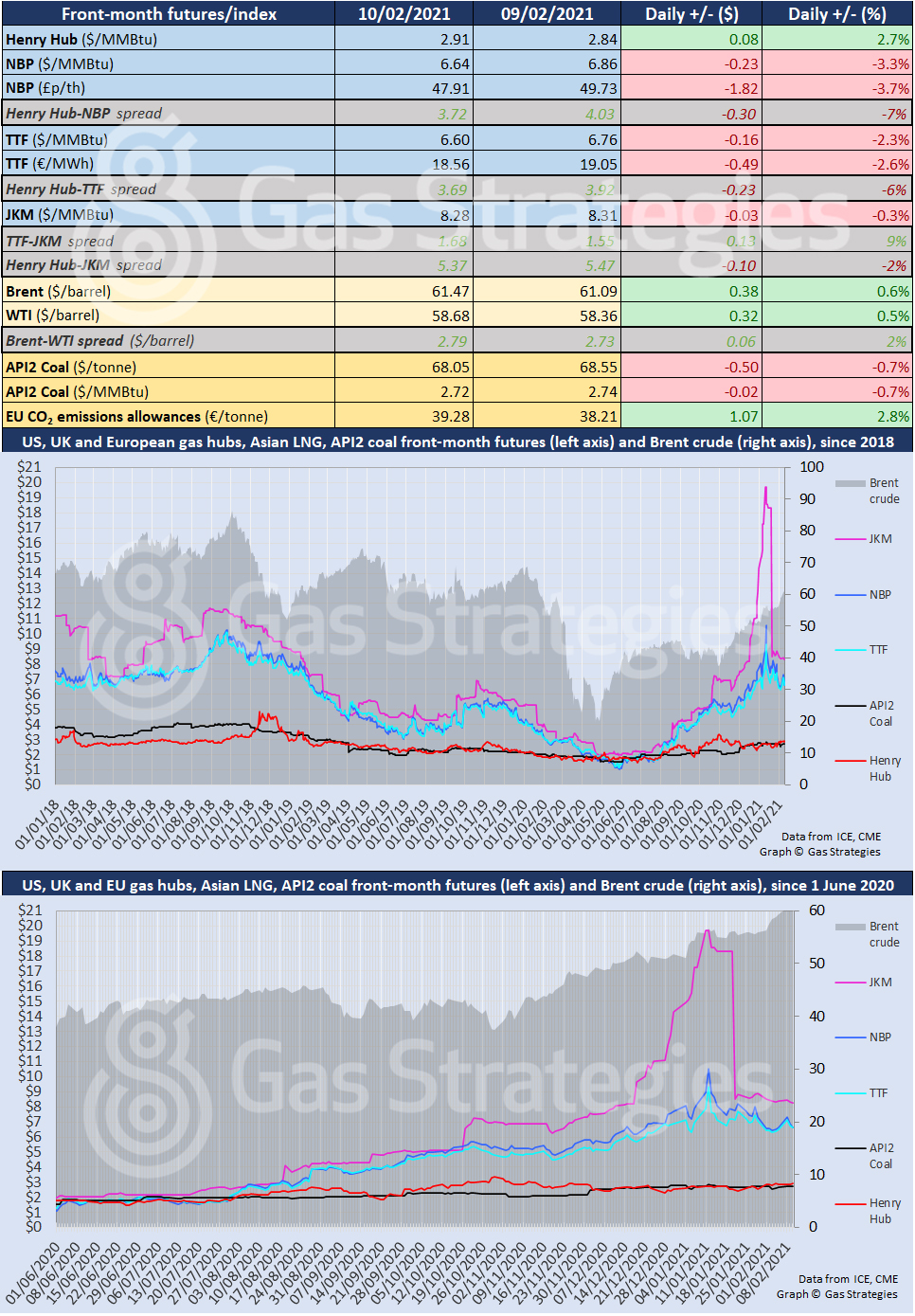

The front-month Brent crude contract made it nine straight days of gains on Wednesday, marking Brent’s longest rally since December 2018 to January 2019. The price rallied by 0.6% to close at USD 61.47/barrel. WTI made it eight days of gains, closing 0.5% higher but remaining in the USD 58/barrel range.

The crude price rally on Wednesday was supported by news from the US Energy Information Administration (EIA), which announced on Tuesday that US crude inventories fell for a third straight week last week to total 469 million barrels – the lowest since March last year.

The European carbon price hit a record high of EUR 39.28/tonne on Wednesday, with the price hitting EUR 40/tonne during trading on Thursday morning. The price has increased by ~18% since the start of the year, with the surge driven by speculative buying interest, as investors bet on a tighter market over the next ten years.

Front-month European gas prices continued to slide amid forecasts of milder weather and ample gas supply. The front-month UK NBP price settled 3.3% lower, and the month-ahead Dutch TTF price slid by 2.3% to settle at the equivalent of USD 6.60/MMBtu. In the US, the front-month Henry Hub price returned to the USD 2.9/MMBtu range after closing 2.7% higher on Wednesday.

CME’s JKM futures contract continued to fall, closing 0.3% lower at USD 8.28/MMBtu.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights reserved.