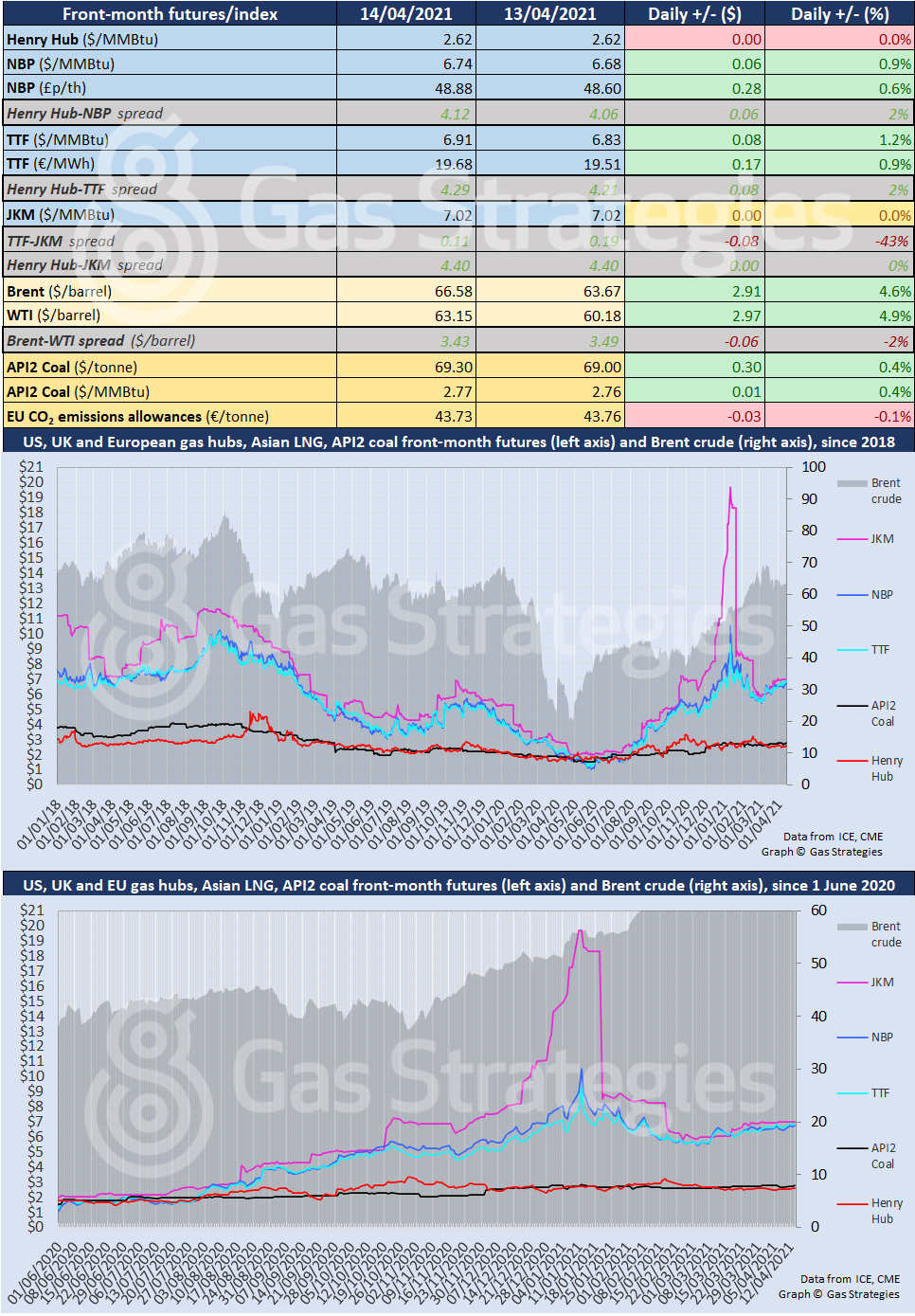

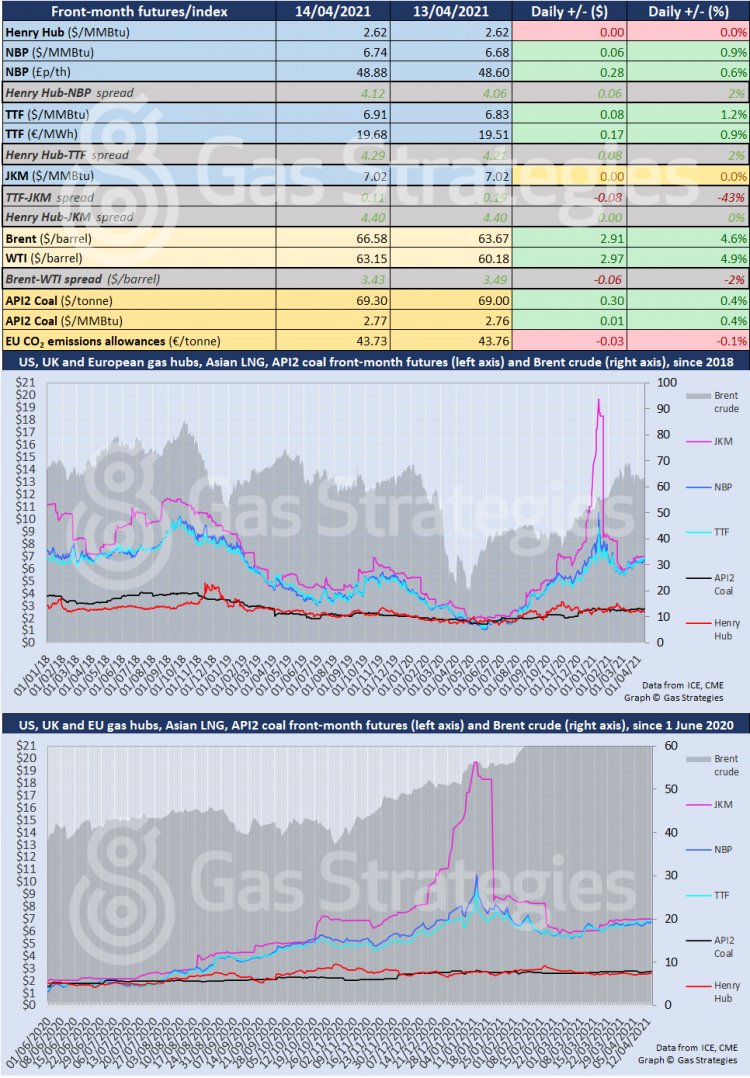

Crude prices settled at their highest since mid-March on Wednesday, with prices rallying on the back of the International Energy Agency (IEA) raising its global oil demand forecast and the US Energy Information Administration (EIA) reporting that US crude inventories have fallen for a third straight week.

The front-month Brent contract closed 4.6% higher on Wednesday to settle in the USD 66/barrel range, with WTI settling in the USD 63/barrel range after rallying by 4.9%.

The crude markers surged on bullish news from the IEA and EIA, with the Paris-based IEA raising its 2021 crude demand forecast by 230,000 barrels/d, compared to its previous forecast in March. The IEA expects global oil demand to increase by 5.7 million barrels/d year-on-year in 2021 to hit 96.7 million barrels/d – still some way off the pre-pandemic levels of ~100 million barrels/d.

The IEA cited improving Covid-19 vaccine rollouts as the reason for lifting its demand forecast, however it aired caution over a demand recovery due to spiralling Covid-19 cases in the likes of Europe, Brazil, the US and India.

"The massive overhang in global oil inventories that built up during last year's COVID-19 demand shock is being worked off, vaccine campaigns are gathering pace and the global economy appears to be on a better footing,” the IEA said in its latest monthly oil market report.

The revised outlook came a day after the Organization of the Petroleum Exporting Countries (OPEC) revised upwards its global crude demand forecast for 2021. The crude cartel now expects demand to increase by 5.95 million barrels/d in 2021 – up 70,000 barrels/d from its previous forecast in March.

Wednesday’s crude price rally was also aided by the EIA reporting that US oil inventories fell by 5.9 million barrels for the week ending 9 April, marking the third consecutive week of draws on storage.

European gas prices also rallied, with the front-month UK NBP and Dutch TTF contracts lifted by supply concerns. With cold weather lingering in the region, storage is still in withdrawal mode in what should now be the injection season, with maintenance on fields in Norway limiting pipeline flows.

The tightening supply outlook and cold weather saw the month-ahead NBP contract close 0.9% higher to settle at the equivalent of USD 6.74/MMBtu. The front-month TTF contract increased by 1.2% to settle at the equivalent of USD 6.91/MMBtu.

The month-ahead JKM contact remained unchanged at USD 7.02/MMBtu, which, along with the rally by the European gas markers, saw the Asian LNG marker’s premium narrow. The TTF-JKM spread fell to just USD 0.11/MMBtu on Wednesday.

In the US, gas benchmark Henry Hub remained at USD 2.62/MMBtu after recording a minor loss.

The European carbon price followed suit, recording a minor loss of 0.1% to settle at EUR 43.73/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close.