European gas prices hit a two-month high on Thursday amid cold weather and tightening supplies, with the rally wiping out the Asian LNG marker JKM’s premium over Dutch gas marker TTF.

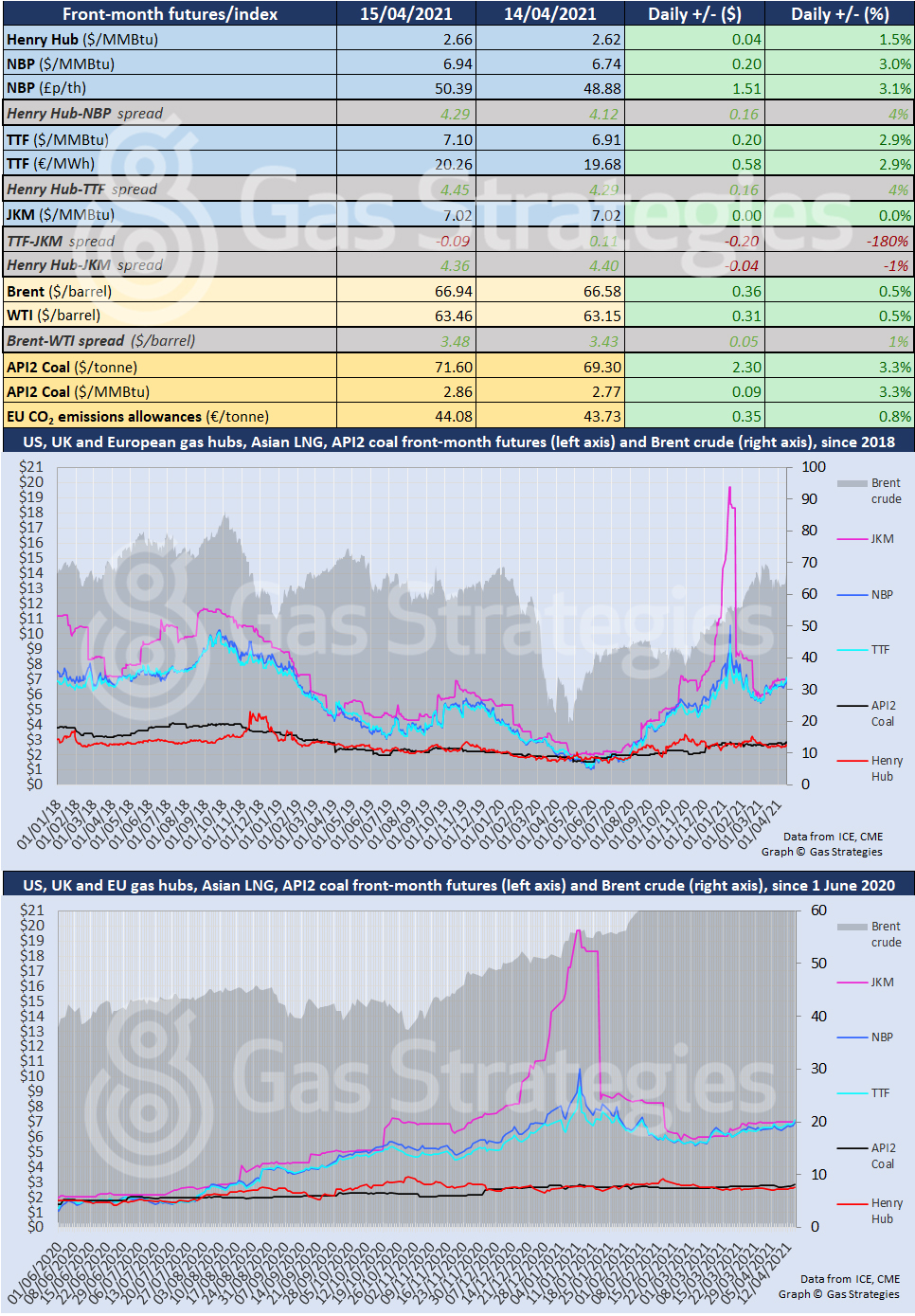

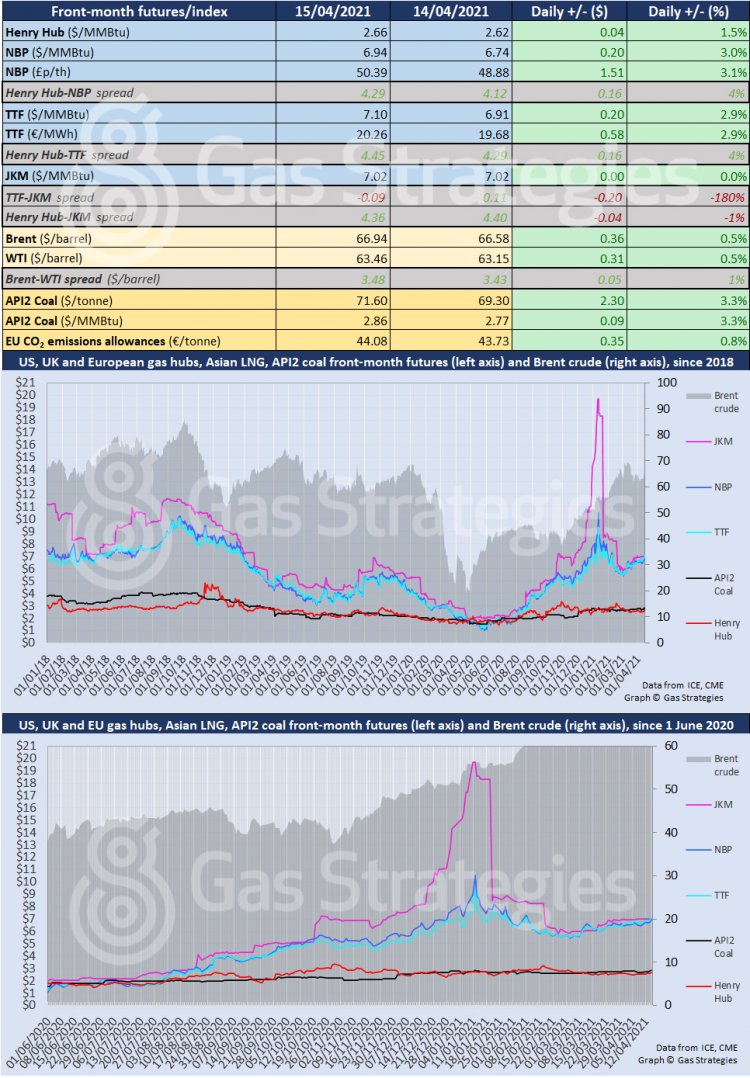

The front-month UK NBP and Dutch TTF contracts rallied by ~3% on Thursday to close at the equivalent of USD 6.94/MMBtu and USD 7.10/MMBtu, respectively.

Cold weather is pushing gas demand in Europe, with supplies tightening due to maintenance on fields in Norway and outages in the UK. Pipeline imports from Norway averaged 299 MMcm/d on Thursday, down on the 308 MMcm/d on Wednesday and the 344 MMcm/d averaged last week, according to EnergyScan. Pipeline flows from Russia fell from 329 MMcm/d on Wednesday to 322 MMcm/d on Thursday.

With pipeline flows limited and winter weather still lingering, Europe is relying on gas from storage in what should now be the injection season. Highlighting how cold April has been in Europe, one trade source told Gas Matters Today that the UK has been experiencing colder weather this month than in December 2020.

“UK temperatures so far in April have been colder than any month average in the previous winter,” the source added.

The rally by the European gas markers eroded JKM’s premium over TTF – which now holds a 0.09/MMBtu premium over the Asian LNG marker. JKM recorded a marginal gain on Thursday but remained at USD 7.02/MMBtu.

The gas price rally also aided the European carbon price which neared previous record highs on Thursday – closing at EUR 44.08/tonne.

In the US, gas benchmark Henry Hub rallied by 1.5% to close at USD 2.66/MMBtu – its highest close since 11 March.

The AP12 coal price also rallied on the cold weather, with the marker hitting a two-year high to close at the equivalent of USD 2.86/MMBtu.

Crude prices continued to rally as the market absorbed the improved oil demand forecasts delivered by the IEA and OPEC this week, with the draw on US crude inventories last week providing further support.

The front-month Brent and WTI contracts increased by 0.5% but remained in the USD 66/barrel and USD 63/barrel range respectively.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.