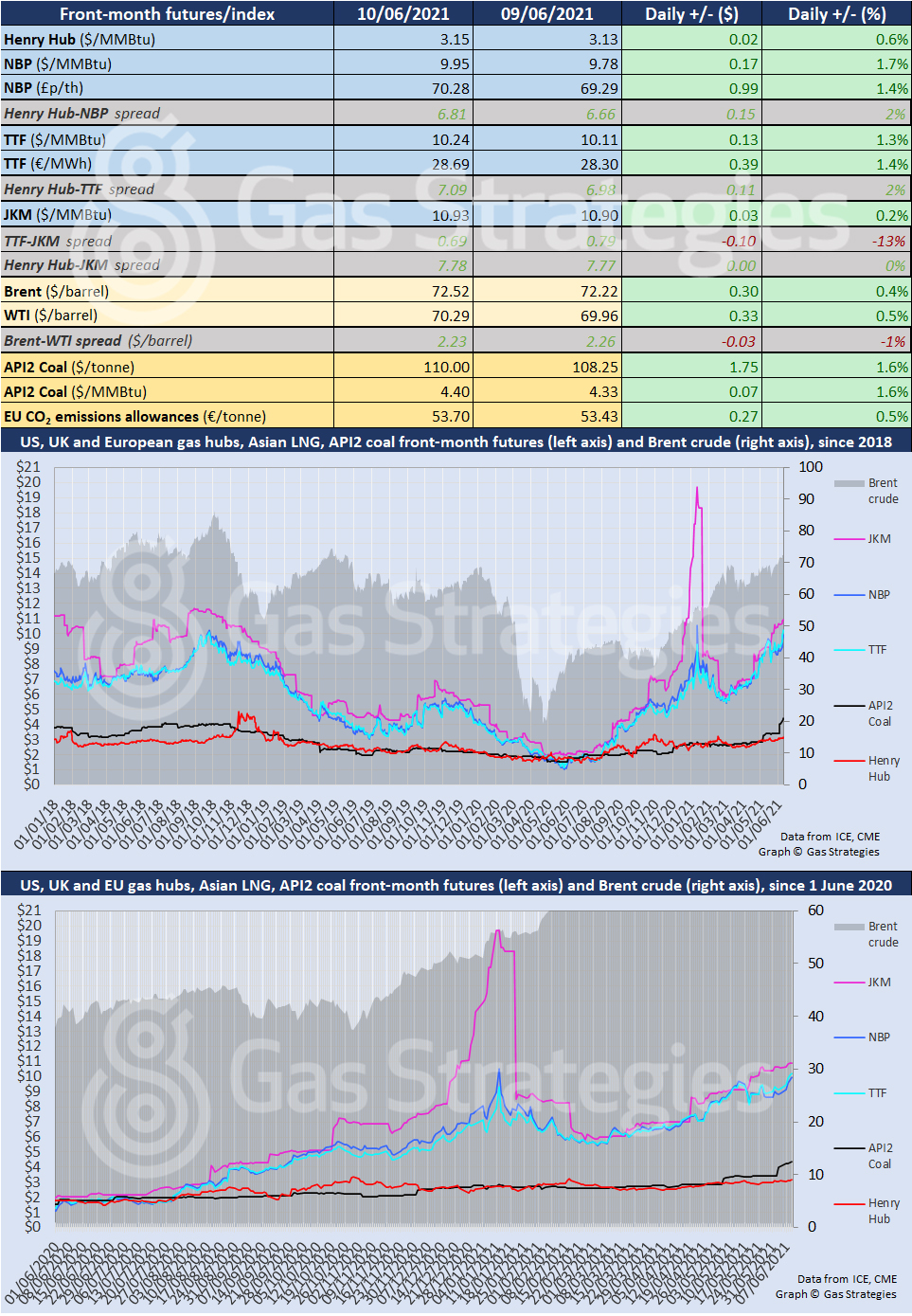

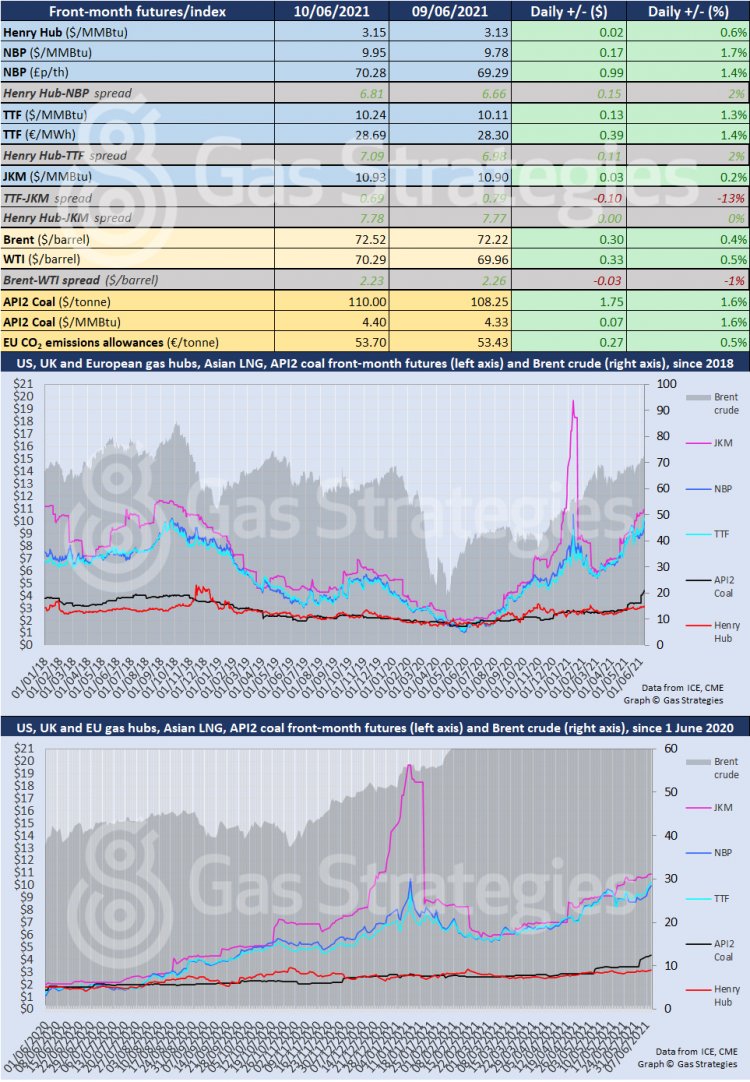

European coal and gas prices continued to surge on Thursday, with the front-month API2 coal contract closing at USD 110/tonne – its highest close since January 2012.

Coal and gas prices in Europe have been rallying on a tight supply outlook, with maintenance in Norway reducing gas flows to the continent and competition for LNG cargoes heating up amid strong demand in Asia. Similarly, strong demand for coal in Asia is helping lift prices in Europe, with supply issues reducing available volumes.

The API2 coal price is up ~USD 24/tonne since the start of June, with the front-month contract settling at its highest in over nine years on Thursday.

The front-month NBP and TTF contracts rallied by 1.7% and 1.3% respectively on Thursday, with the UK benchmark closing at the equivalent of USD 9.95/MMBtu and TTF settling at USD 10.24/MMBtu.

The rally helped lift the front-month JKM contract and the European carbon price. JKM rallied by 0.2% to close at USD 10.93/MMBtu – its highest close since 20 January – however the rally by TTF saw JKM's premium over the Dutch marker cut to USD 0.69/MMBtu on Thursday.

The European carbon price closed at EUR 53.7/tonne – its highest close since 17 May, with Thurday’s rally also prompted by the strengthening European coal price.

In the US, gas benchmark Henry Hub closed 0.6% higher to settle at USD 3.15/MMBtu. Henry Hub has been rallying on strong demand amid robust LNG and pipeline exports and warmer weather driving domestic demand.

Crude prices dipped during trading on Thursday after the Biden administration announced that it had lifted US sanctions against several Iranian energy firms and three former Iranian officials.

Washington said the move was a routine administrative action and not related to negotiations over a new nuclear deal – which could see Iran increase oil exports. A fresh round of talks over a new nuclear deal are expected to start this weekend in Vienna.

After dipping during the session, Brent and WTI closed 0.4% and 0.5% higher respectively on Thursday.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.