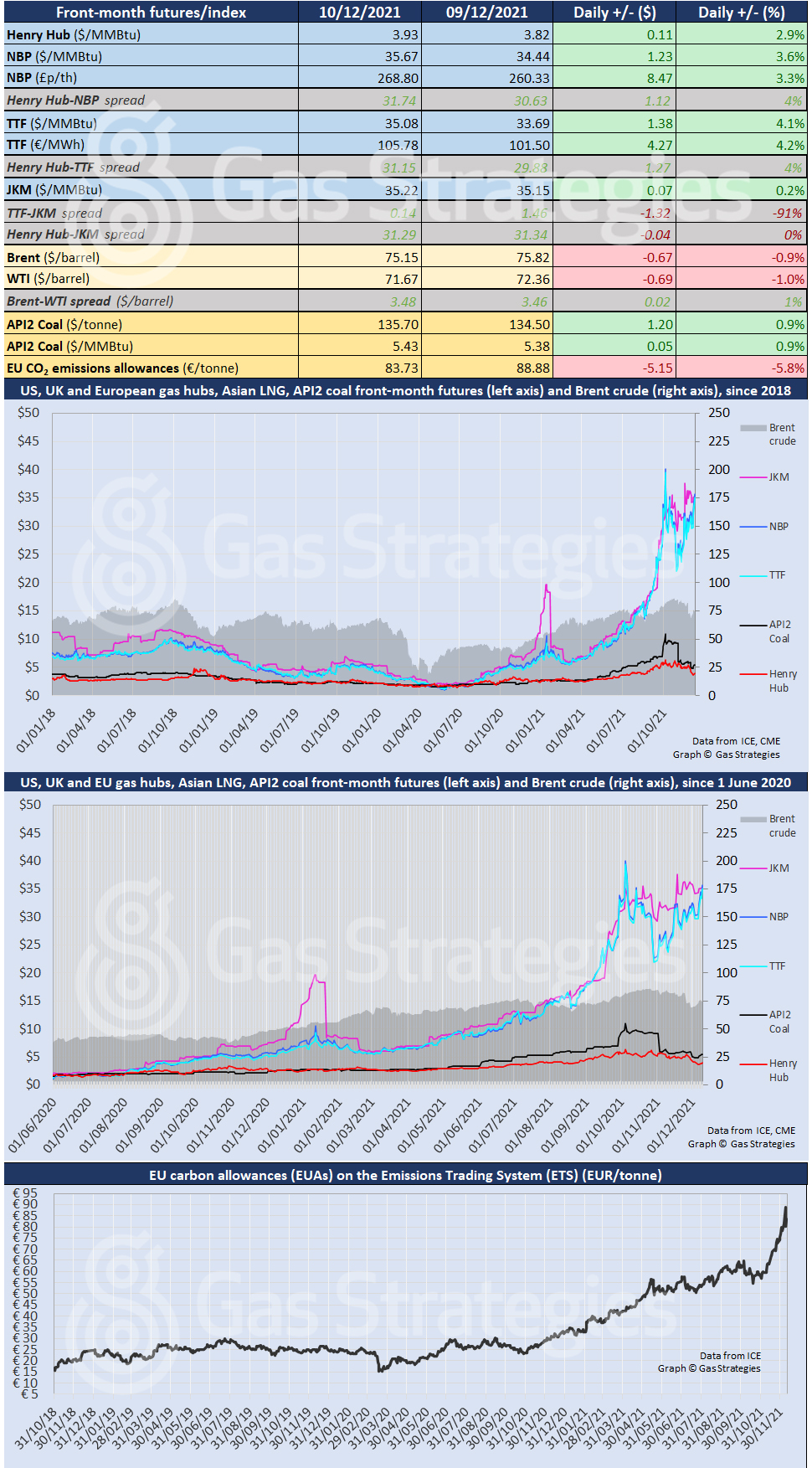

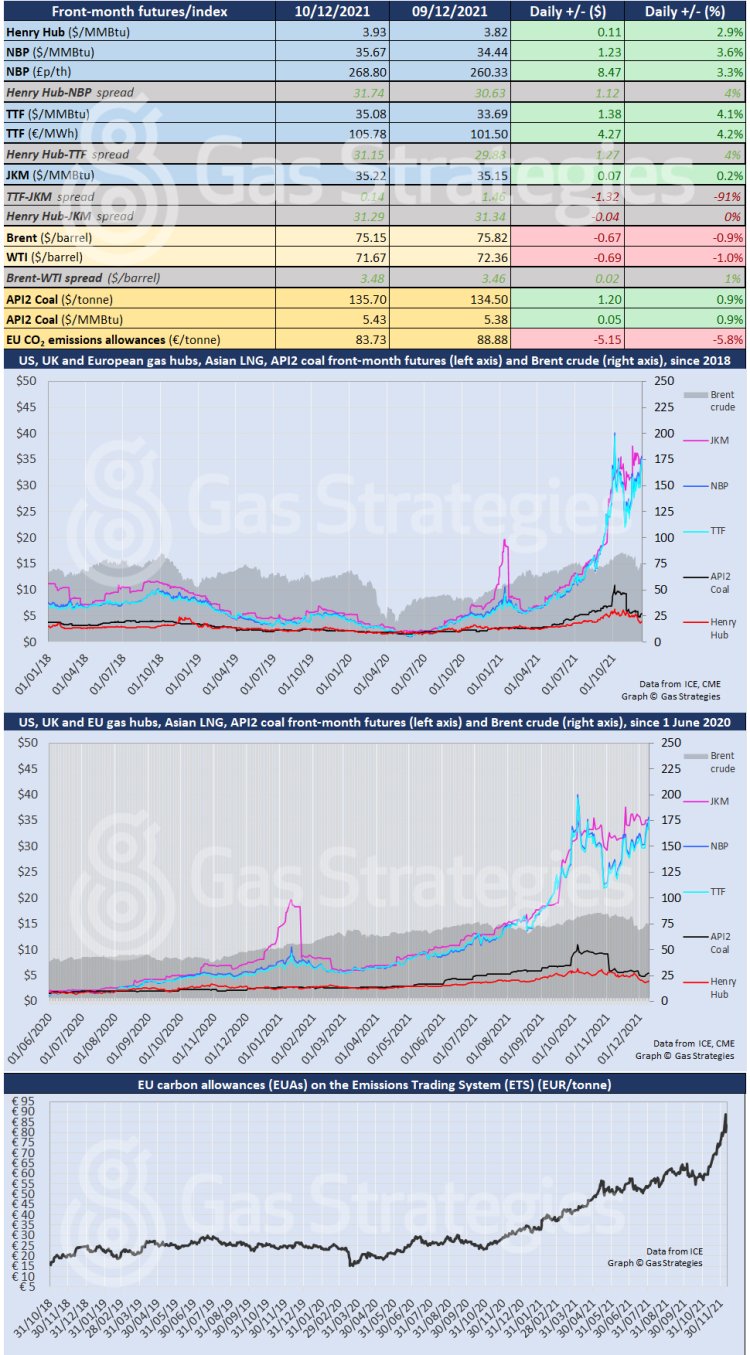

It was a mixed end to the week for crude and gas prices, with oil falling back, as concerns re-emerged over the potential impact of the Covid-19 Omicron variant on energy demand in key markets, while Europe’s gas benchmarks were once again influenced by fears over supplies this winter.

On the oil front, Brent shed 67 cents to USD 75.15/barrel, while the WTI was down by 69 cents to USD 71.67/barrel. Despite optimism earlier in the week that Omicron’s impact on demand could be minimal, the mood turned more pessimistic on Friday, as many governments took the decision to speed up their booster vaccination programmes to tackle the variant’s spread.

In Europe, raised tensions between the EU, US and Russia over Ukraine pushed gas prices higher, as the continent continued to face low gas storage this winter, with Gas Infrastructure Europe showing levels at 62.8% full – though temperatures in some regions were expected to be mild for this time of year on Sunday and into the new working week, easing demand.

The Dutch TTF front-month contract gained USD 1.38/MMBtu on Friday, settling at USD 35.08/MMBtu, while the UK NBP was up USD 1.23/MMBtu to USD 35.67/MMBtu, with the TTF’s discount to the Asian JKM LNG market narrowing by USD 1.32/MMBtu to just 14 cents, as the JKM was up by just 7 cents on the day to USD 35.22/MMBtu.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.