Natural gas prices in Europe and Asia continued their months-long decline from the soaring peaks of 2022 last week – despite a brief rally in the second half – falling by around a fifth week-on-week.

Natural gas prices in Europe and Asia continued their months-long decline from the soaring peaks of 2022 last week – despite a brief rally in the second half – falling by around a fifth week-on-week.

Most price drivers continued to exert downward pressure, the most significant being the culmination of the winter heating season and Europe’s success in adapting to the impacts of Russia's weaponisation of energy supplies. The vernal equinox, marking the start of astronomical spring in the northern hemisphere, happens at 21:24 UTC on Monday.

Also playing a role were the re-opening of one of the French LNG import terminals – at Dunkerque – and an easing of concerns over French nuclear power, despite expansion of an inspection programme following cracks found in a pipe at one reactor. Three other French LNG terminals remain blocked by industrial action.

The significant falls in gas prices on Friday were part of a broader decline in energy prices, with Asia’s JKM marker once again remaining the exception, with no change from Thursday.

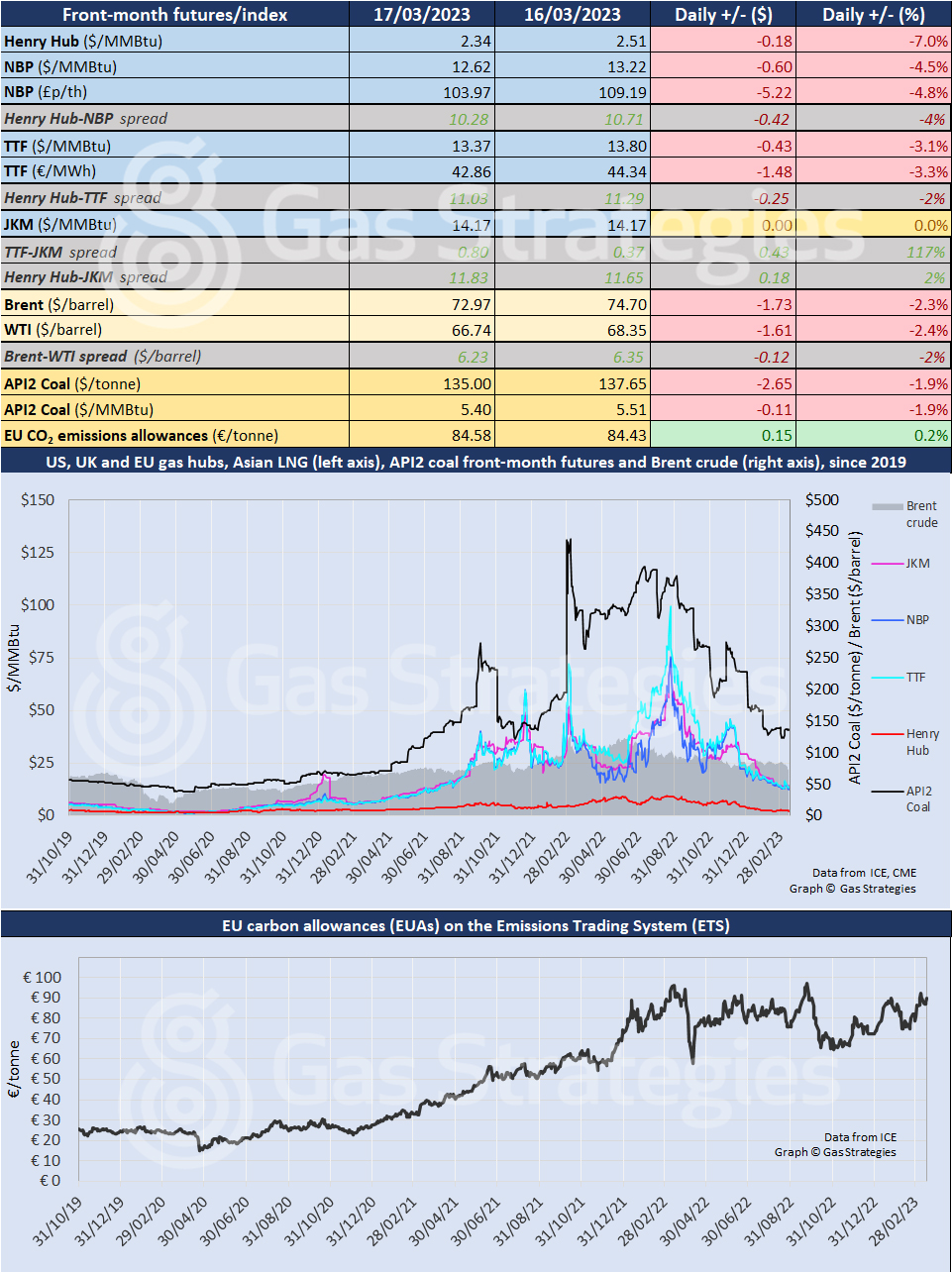

In continental Europe, the Dutch TTF marker fell 3.3% on Friday, from EUR 44.34/MWh (USD 13.80/MMBtu) on Thursday to EUR 42.86/MWh (USD 13.37/MMBtu). The week-on-week change was a fall of 19.2%, from EUR 52.86/MWh (USD 16.51/MMBtu) on Friday 10 March. Further falls are likely this week with temperatures forecast above seasonal norms.

Moreover, the European Commission said on Monday that it proposed prolonging emergency legislation to reduce gas demand by 15% for another 12 months when the existing regulation, agreed in July 2022, expires at the end of this month. The proposals – part of a strategy to prepare for winter 2023/24 – will be discussed by EU energy ministers on 28 March.

The UK’s NBP was down 4.8% from 109.19 p/therm (USD 13.22/MMBtu) on Thursday to 103.97 p/therm (USD 12.62/MMBtu). Week-on-week it fell by 22.3%, from 133.56 p/therm (USD 16.08/MMBtu).

In Asia, the JKM LNG marker remained flat day-on-day at USD 14.17/MMBtu after declining for most of 2023. Week-on-week it was down a tiny 0.07%, with weakening demand in Europe offset by rising buyer interest in Asia. The TTF-JKM spread was up to USD 0.80/MMBtu on Friday, from USD 0.37/MMBtu the previous day – a major reversal from USD -2.35/MMBtu a week ago.

In the US, Henry Hub fell back 7.0% from USD 2.51/MMBtu on Thursday to USD 2.34/MMBtu, down 3.9% from USD 2.43/MMBtu a week earlier.

Oil prices also fell on Thursday, with Brent down 2.3% from USD 74.70/barrel on Wednesday to USD 72.97/barrel on Friday, and WTI down 2.4% from USD 68.35/barrel to USD 66.74/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.