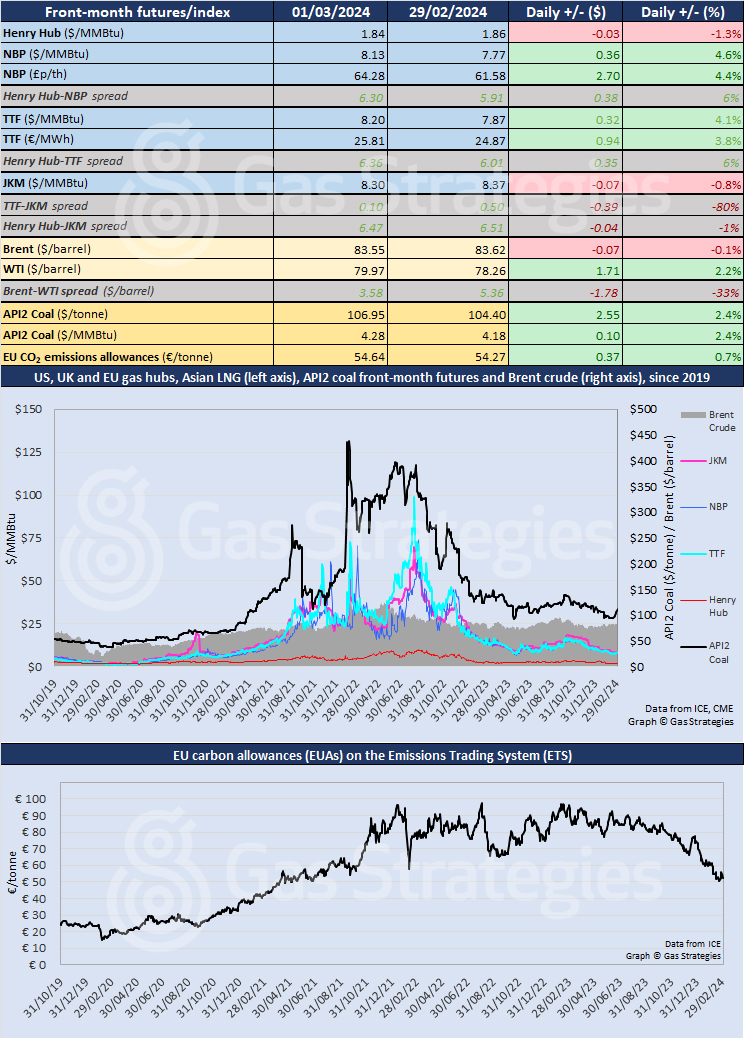

European natural gas futures continued to see-saw on Friday, reversing their falls in the previous trading session, on the first day of meteorological spring.

In Continental Europe, TTF rose by 4.1%, from USD 7.87/MMBtu on Thursday to USD 8.20/MMBtu on Friday. In the UK, NBP rose by 4.6%, from USD 7.77/MMBtu on Thursday to USD 8.13/MMBtu on Friday.

While prices opened lower again on Monday, the straight-line decline that has taken place since October appears to be levelling off, though at this stage it is too early to be definitive. Prices were climbing again by lunchtime on Monday.

The weather in north-west Europe has been less mild in recent days than in recent weeks and more chilly weather is forecast for the coming week, notably in Germany.

Withdrawals from European Union storage were significant on several days last week, while UK storage has been on a downward trend for the past 10 days after a week of rises. That said, storage levels remain much higher than normal for the time of year in Europe as a whole.

Warmest Februarys

In the UK, the Meteorological Office has confirmed that “England and Wales had their respective warmest Februarys on record … in what was a mild and wet month for many”. The UK as a whole experienced its second-warmest February in a series from 1884, with the 10 warmest Februarys including 2024, 2023, 2022 and 2019.

“The UK’s observations clearly show winters are getting warmer, and they are also getting wetter since as the atmosphere heats up, it has an increased capacity to hold moisture,” said the Met Office’s Mike Kendon.

In Asia, JKM fell again – by 0.8% – from USD 8.37/MMBtu on Thursday to USD 8.30/MMBtu on Friday, putting it almost on parity with TTF. The TTF-JKM spread is now just USD 0.10/MMBtu.

In the US, the April Henry Hub contract fell by another 1.3%, from USD 1.86/MMBtu on Thursday to USD 1.84/MMBtu on Friday, with mild weather forecast into the weekend.

In early trading on Monday, the price was up 6.5% to USD 1.95/MMBtu – the closest that the front-month contract has been to USD 2/MMBtu in almost a month.

The price jump came amid news that EQT Corporation is cutting production by 1 Bcf/d from late February and throughout March, equivalent to around 1% of total US output. The company said the curtailment was "in response to the current low natural gas price environment resulting from warm winter weather and consequent elevated storage inventories".

Brent and WTI crude oil futures diverged significantly, with the former edging down by 0.1%, from USD 83.62/barrel on Thursday to USD 83.55/barrel on Friday, while the latter rose by 2.2%, from USD 78.26/barrel to USD 79.97/barrel. The Brent-WTI spread narrowed by a third, from USD 5.36/barrel to USD 3.58/barrel.

The Brent price has barely moved for a week, having traded in a range of USD 83.53-83.68/barrel. Both Brent and WTI were down by about half a percentage point on Monday by lunchtime in London.

European coal prices rose in line with rising gas prices, with API2 up 2.4%, from USD 4.18/MMBtu on Thursday to USD 4.28/MMBtu on Friday.

Five consecutive rises saw API2 climb by 8.2% over the course of last week, while TTF climbed by 7.5% over the same period.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.