Brent crude oil futures were back above USD 90/barrel on Wednesday amid growing concerns on the part of US intelligence sources that Iran may be about to mount a direct attack on Israel. Price movements were muted in other energy markets around the globe.

US president Joe Biden promised “iron-clad support” for Israel, following reports that Iran’s supreme leader, Ayatollah Ali Khamenei, had repeated his warning that Israel would be punished for an attack on an Iranian embassy compound in the Syrian capital of Damascus at the start of this month.

Iran has repeatedly blamed Israel for the air strike, which killed seven people, including senior military commanders, but Israel has so far not commented on its alleged involvement.

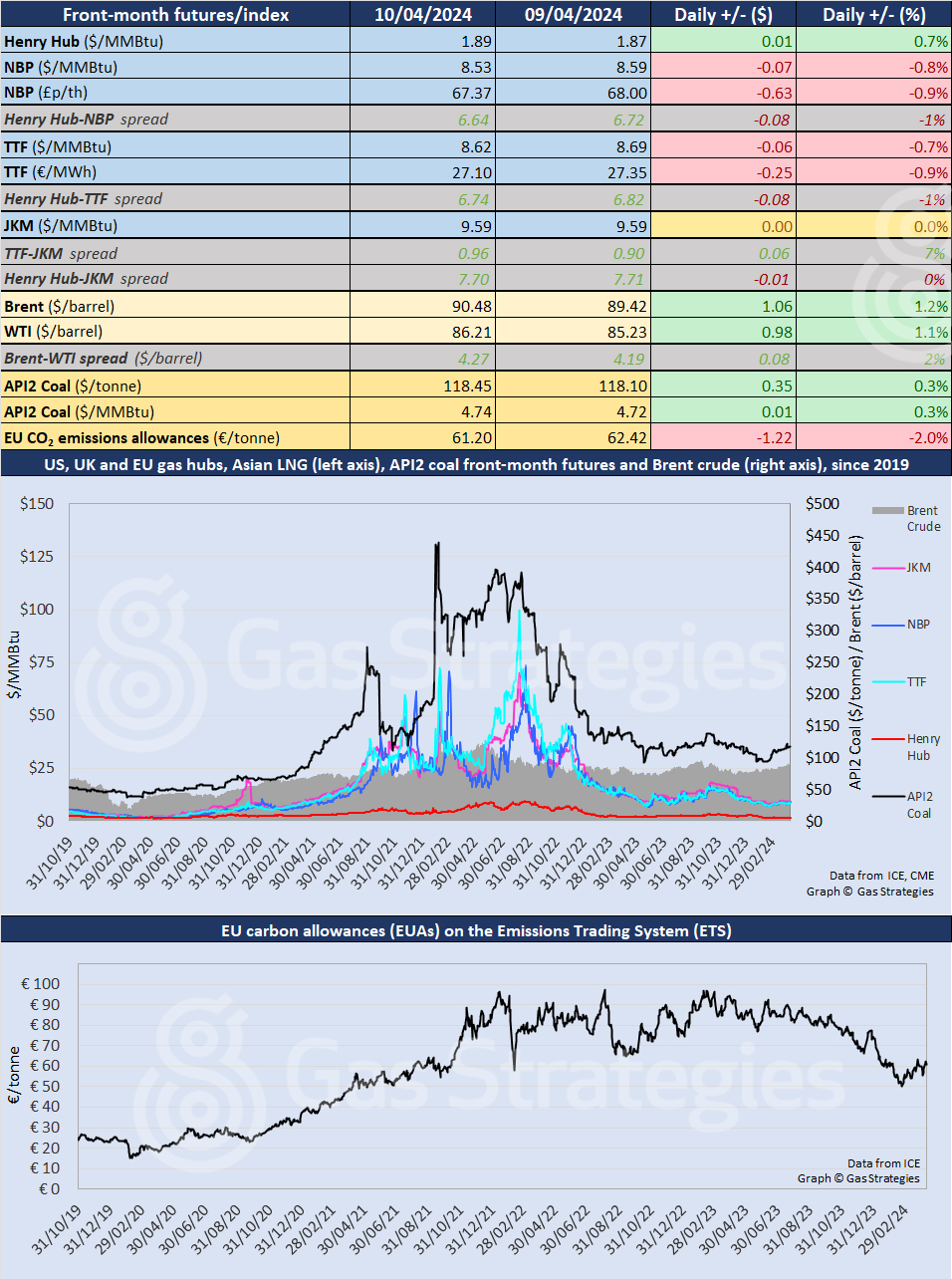

The May Brent crude contract closed up 1.2%, from USD 89.42/barrel on Tuesday to USD 90.48/barrel on Wednesday, taking the price to slightly above where it closed on Monday. WTI was up 1.1%, from USD 85.23/barrel to USD 86.21/barrel. Prices were down by around half a percentage point by Thursday lunchtime in London.

Brent has been oscillating around USD 90/barrel since the start of April, appearing to have settled – at least for now – into a new dynamic equilibrium, significantly above the USD 77-80/barrel range that persisted for the first weeks of 2024.

The US Energy Information Administration (EIA) said earlier this week it expected Brent to average USD 90/barrel in the second quarter of 2024 and USD 89/barrel for the whole year.

European natural gas futures fell for the second session in a row, maintaining the sawtooth pattern that has characterised trading over recent weeks, with the underlying trend appearing flat.

In continental Europe, the May TTF contract closed down 0.7%, from USD 8.69/MMBtu on Tuesday to USD 8.62/MMBtu on Wednesday. In the UK, NBP futures closed down 0.8%, from USD 8.59/MMBtu to USD 8.53/MMBtu.

In Asia, the JKM LNG price maintained its run of stability, remaining flat at USD 9.59/MMBtu. The TTF-JKM spread is now just under a dollar.

In the US, front-month Henry Hub rose for the fourth consecutive session, closing up 0.7%, from USD 1.87/MMBtu on Tuesday to USD 1.89/MMBtu on Wednesday, as traders awaited the latest storage data from the EIA, due out later today. The market expectation is for a small injection.

Feedgas volumes to the Freeport LNG export facility are on the rise, suggesting the second of three liquefaction trains has restarted following repairs and maintenance. Meanwhile, US gas output is at around 98 Bcf/d, significantly down on levels earlier this year as some producers implement curbs in response to low prices.

European coal prices edged up on Wednesday, with API2 rising 0.3% to USD 4.74/MMBtu.

Carbon prices partially reversed recent sharp gains, with a 2% fall in the price of EU emissions allowances to EUR 61.20/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.