The topsy-turvy side of Middle Eastern geopolitics was on display yesterday as major news outlets reported with undisguised astonishment that oil prices had fallen in the wake of Iran’s unprecedented direct attack on Israel on Saturday night.

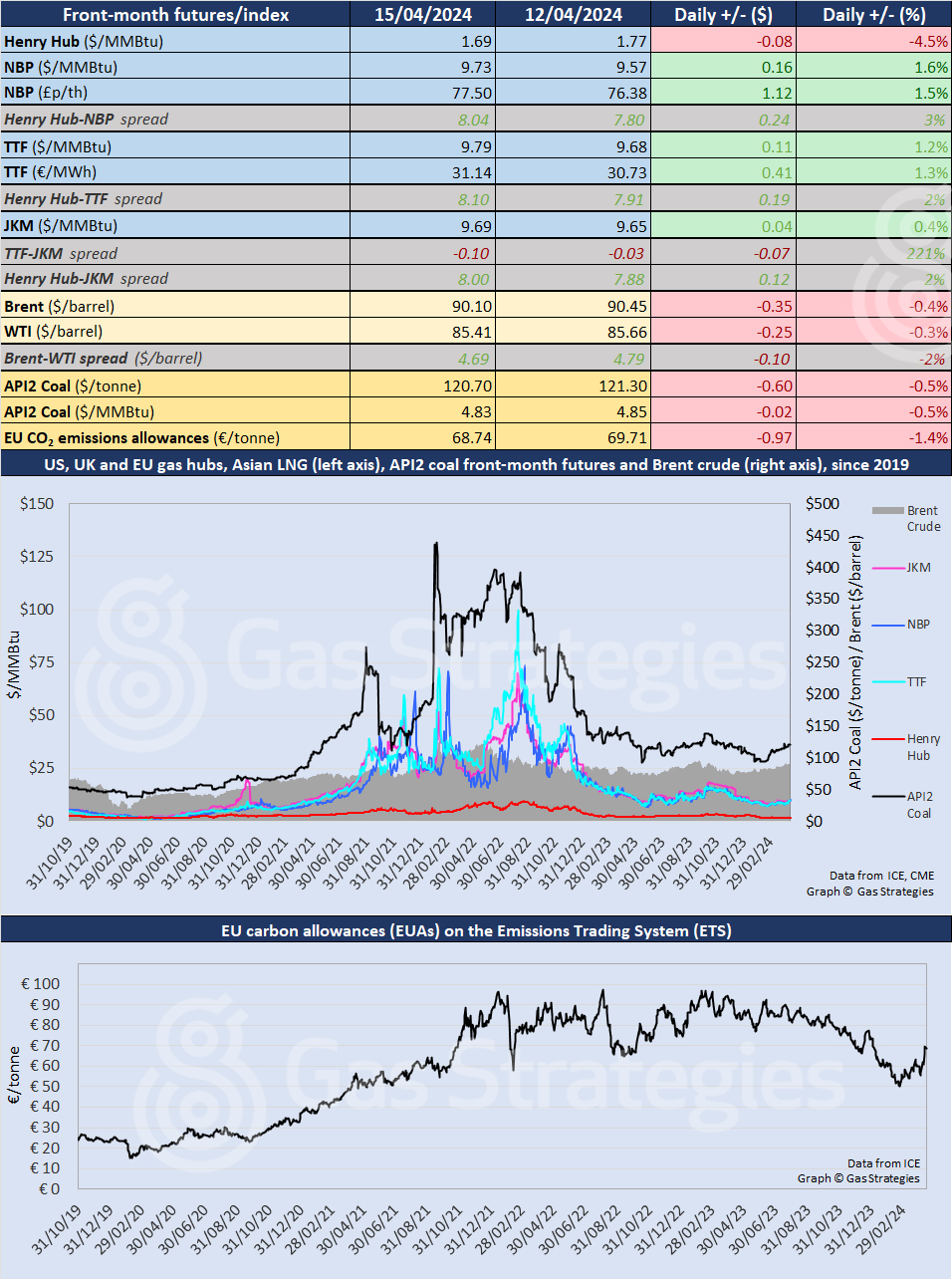

The June Brent contract fell by 0.4%, from USD 90.45/barrel on Friday to USD 90.10/barrel on Monday, while WTI was down 0.3%, from USD 85.66/barrel to USD 85.41/barrel. That said, it is worth noting that prices briefly spiked when the attack was first reported.

The simple truth is that markets had priced in a more worrying scenario than that which transpired, with the general response to Iran’s attack appearing to be “is that the best you can do?”. Reportedly, more than 99% of the drones and projectiles that Iran lobbed at Israel were shot down or failed to make the distance.

However, these remain early days in what everyone agrees is a dangerous new phase in the long-running antagonism between Iran and Israel and the world waits to see what Israel will do next.

The reality is that oil prices have been trading in a band much higher than the range they were in at the start of 2024. Brent has been oscillating around USD 90/barrel for over a fortnight, which compares with a range of USD 76-81/barrel in the first weeks of the year – an increase of around 15%.

READ Strait of Hormuz in focus after Iran's attack on Israel

Similarly, European natural gas futures have taken in their stride reported threats around a possible blockade of the Strait of Hormuz, the conduit for LNG supplies from Qatar and the UAE and around a fifth of the world’s crude oil supply.

Closing the strait is not a simple matter as it is wider than many realise and any credible threat would almost certainly provoke a response from Western allies, not least because of the threat to oil supply.

In continental Europe, front-month TTF was up by 1.2%, from USD 9.68/MMBtu on Friday to USD 9.79/MMBtu on Monday and the price continued to rise on Tuesday morning, up by around another 3% by lunchtime in London.

In the UK, the trajectory was similar, with NBP up 1.6%, from USD 9.57/MMBtu to USD 9.73/MMBtu, and rising further on Tuesday morning.

As with oil, there has been a structural shift upwards in recent months, especially since the start of April. Yesterday’s TTF close was a 36% increase on the low point in late February.

In Asia, the JKM LNG price remained rangebound, up 0.4%, from USD 9.65/MMBtu to USD 9.69/MMBtu, close to parity with TTF and NBP.

The question now – especially for price-sensitive LNG buyers in Asia – is whether these prices will move back into double figures in coming days or weeks.

In the US, front-month Henry Hub was down 4.5%, from USD 1.77/MMBtu on Friday to USD 1.69/MMBtu on Monday, with demand dampened by mild weather and supplies to LNG export plants down. A substantial injection into storage is anticipated in government data to be published on Thursday.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.