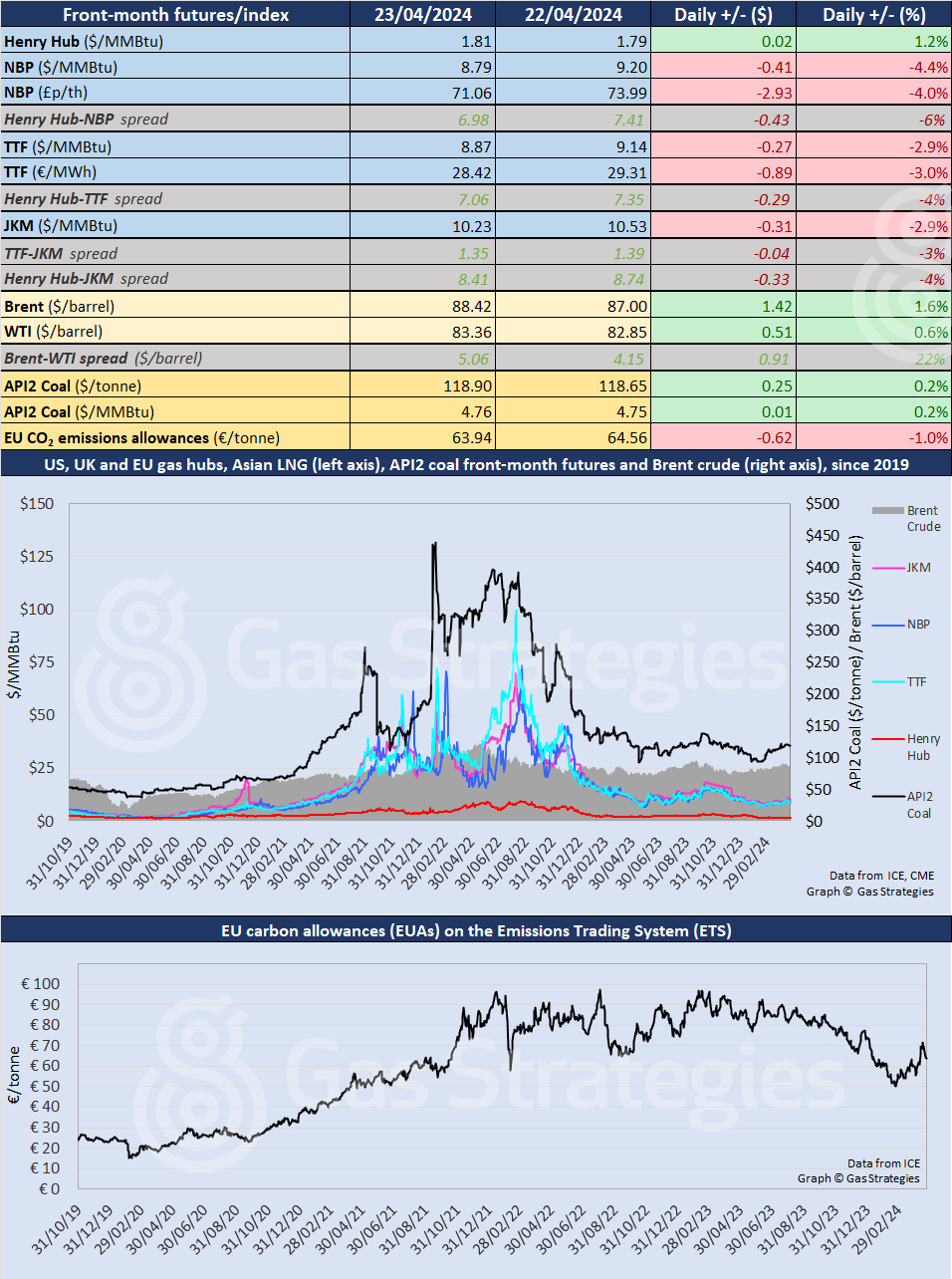

Natural gas futures in Europe continued their descent on Tuesday, with a third consecutive fall taking them below USD 9/MMBtu. This left prices around 12% lower than they closed on Thursday of last week, just before Israel made its underwhelming retaliatory strike – still not confirmed by Israel itself – against Iran.

In continental Europe, the May TTF contract closed down 2.9%, from USD 9.14/MMBtu on Monday to USD 8.87/MMBtu on Tuesday. The price was up a little in volatile trading on Wednesday morning.

In the UK, NBP fell a little more sharply, down 4.4%, from USD 9.20/MMBtu to USD 8.79/MMBtu, and its trajectory on Wednesday morning was similar to that of TTF.

The falls reflect declining geopolitical risk, with no further developments in the stand-off between Israel and Iran, and more military and economic aid on its way to Ukraine. As expected, the Democrat-controlled US Senate yesterday approved the USD 61 billion aid package for Ukraine that was passed by the House of Representatives over the weekend.

While there has no more direct conflict between Iran and Israel, proxy conflict continues, with Al Jazeera reporting that Iran-backed Hezbollah has mounted a drone attack deep into Israel from Lebanon – in retaliation for the killing of one of its fighters in southern Lebanon.

The Asian JKM LNG price is also down significantly since last Thursday, having fallen by 6% to a little over USD 10/MMBtu, an important threshold for price-sensitive buyers in South Asia and China. JKM has been less volatile than TTF and NBP for some time.

The price closed at USD 10.23/MMBtu on Tuesday, down 2.9% from USD 10.53/MMBtu on Monday. A TTF-JKM spread of USD 1.35/MMBtu makes Asia a more attractive market for LNG cargoes than Europe, subject to shipping costs.

US gas futures and crude oil futures bucked the downward trend, with other drivers in play.

In the US, Henry Hub was up for a second consecutive session, rising by 1.2%, from USD 1.79/MMBtu on Monday to USD 1.81/MMBtu on Tuesday, as supply was impacted by pipeline maintenance and demand boosted by increased flows to LNG export plants.

Crude oil futures edged upwards as macroeconomic factors raised concerns over demand, with Brent up 1.6% to USD 88.42/barrel while WTI closed up 0.6% to USD 83.36/barrel.

In an interview with Barron’s, Daniel Yergin, vice chairman of S&P Global, gave his take on how oil prices have been responding to geopolitical developments in the Middle East, making the point that the turmoil has had little actual impact on supply.

“You saw some disruption that came with the Houthis disrupting shipping through the Red Sea, but the market adjusted,” he says. “You saw a disruption coming, going back with the restrictions on Russian oil. But the big question will be, will there be stability or is it just another calm between the storms?”

He adds: “We’ve certainly seen a geopolitical premium go into the price and then, at least after the exchange of missiles between Iran and Israel, revert to where it was in late March. That reflects the reality of the forces of supply and demand.

“There is no disruption of oil occurring and less prospect of disruption than it seemed a week ago.”

While the risk of miscalculation remains large, says Yergin, US shale oil is playing a key stabilising role, with the US now the world’s largest producer by far.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.